Downloaded 323 times

![References

Carter, C. O., 1980.

4,242,531.

Lummus Technology, 2010.

US, Patent No.

s.l.:Provided by Lummus

on August, 24th 2010.

Carter, C. O., 1985.

Lummus Technology, 2010.

s.l.:Provided by Lummus on August, 24th, 2010.

Chodorge, J. A., Cosyns, J., Commereuc, B. & Torck, B., 1997.

Propylene Production from Butenes and Ethylene.

, Spring.

Delaude, L. & Noels, A. F., 2007. Metathesis Section. In:

s.l.:WileyInterscience.

Drake, C. A. & Reusser, R. E., 1986.

US, Patent No. 4,575,575.

Mol, J. C., 2004. Industrial Applications of Olefin Metathesis.

213(1), pp. 39-45.

Network China Industrial Information, n.d.

[Online]

Available at: www.chyxx.com

[Accessed 10 March 2012].

Senetar, J. J. & Glover, B. K., 2010.

Dwyer, C. L., 2006. Metathesis of Olefins. In: G. P. Chiusoli & P.

M. Maitlis, eds.

s.l.:Royal Society of Chemistry, pp. 201-217.

Stanley, S., 2009. Cover Story – Ethylene Enhancement.

, February.

Eisele, P. & Killpack, R., 2002. Propene Section. In:

s.l.:Wiley-Interscience.

Sumner, C., 2009.

Gartside, R. J. & Greene, M. I., 2007.

No. 7,525,007 B2.

US, Patent

US,

Patent No. 7,214,841 B2.

Takai, T. & Kubota, T., 2010.

Patent No. 2010/0145126 A1.

US,

Gartside, R. J., Greene, M. I. & Jones, Q. J., 2004.

US, Patent No. 6,777,582 B2.

Gartside, R. J. & Ramachandran, B., 2010.

Weidert, D. J., 2000.

s.l., AIChE 2000 Spring Meeting.

Zinger, S., 2005. One-purpose propylene production.

, Q3.

Hildreth, J. M., Dukandar, K. N. & Venner, R. M., 2009.

Hydrocarbon Processing, 2005.

s.l.:Gulf Publishing.

Intratec | References

Lummus Technology, 2009.

[Online]

Available at:

www.cbi.com/images/uploads/tech_sheets/Olefins.pdf

[Accessed 20 March 2012].

FREE SAMPLE

37](https://image.slidesharecdn.com/tec001a-preview-120402190638-phpapp01/75/Technology-Economics-Propylene-via-Metathesis-41-2048.jpg)

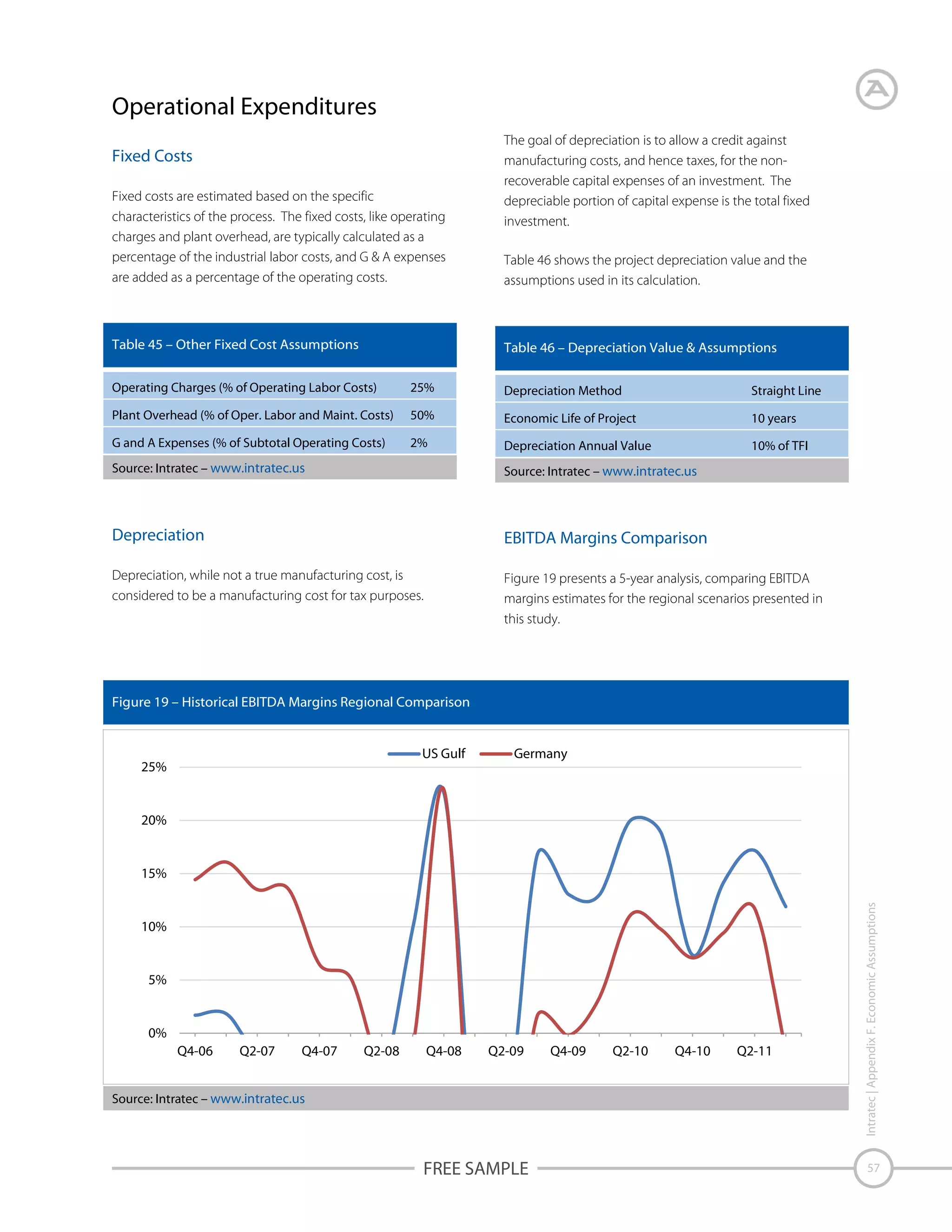

This study analyzes the production of propylene via metathesis from ethylene and butenes. It provides an overview of the metathesis technology and economics of a process similar to the CB&I Lummus OCT process. Capital and operating costs are presented for a plant constructed in the US Gulf and Germany. Alternative ways to produce propylene via butenes-only or ethylene-only metathesis are also discussed.