The UK employeebenefits landscape (November 2025) 1

The UK employee benefits landscape

Data and insights to inform your employee

benefits decision-making

November 2025

2.

The UK employeebenefits landscape (November 2025) 2

What’s inside?

Technology

6

The UK employee benefits landscape 2

Introduction

3 10 Health

16 Wellbeing

37 Next steps

21 Protection 27 Pensions

3.

The UK employeebenefits landscape 3

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Introduction

What this report’s all about

In November 2023, we revealed the results of the first Broadstone Employee Benefits Survey. Our goal? To

capture a detailed picture of the employee benefits market and share our insights with you – the people

working in employee benefits strategy, selection, and management. With a constantly shifting landscape,

we decided now was the time to do it again. This report is a summary of our findings in 2025.

At Broadstone, we offer expert employee benefits advice and the technology solutions to deliver an effective,

efficient, and engaging benefits programme for your people. That’s why it’s vital we monitor the market, the

opportunities and challenges it presents, and its emerging trends and expectations. This survey helps us:

ب Understand employer priorities and benefits-related decision-making at a macro-level

ب Identify and track trends in employee benefits

ب Provide our clients with relevant, up-to-date advice

Why you should read this report

If you work in employee benefits, this report is for you. Business is full of ever-changing challenges, from

recruitment and retention to employee wellbeing and cost control, so understanding the bigger picture is crucial.

Whether you’re an HR director, head of rewards and benefits, or a pension trustee, you’ll find valuable information

to help develop and refine your organisation’s future employee benefits strategy.

Manager

Director

Head of

C-Suite

Business Partner

Advisor/Specialist

Other

19%

32%

19%

10%

9%

7%

5%

60+

Questions

48%

250+ employees

61%

HR, Reward or

Benefits role

200

responses

4.

The UK employeebenefits landscape 4

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Introduction

Recent challenges, future priorities

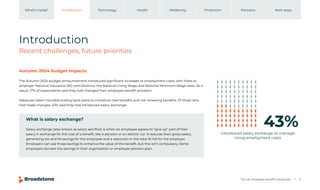

Autumn 2024 budget impacts

The Autumn 2024 budget announcement introduced significant increases to employment costs, with hikes to

employer National Insurance (NI) contributions, the National Living Wage and National Minimum Wage rates. As a

result, 17% of respondents said they had changed their employee benefit provision.

Measures taken included scaling back plans to introduce new benefits and not renewing benefits. Of those who

had made changes, 43% said they had introduced salary exchange.

What is salary exchange?

Salary exchange (also known as salary sacrifice) is when an employee agrees to “give up” part of their

salary in exchange for the cost of a benefit, like a pension or an electric car. It reduces their gross salary,

generating tax and NI savings for the employee and a reduction in the total NI bill for the employer.

Employers can use those savings to enhance the value of the benefit, but this isn’t compulsory. Some

employers reinvest the savings in their organisation or employee pension plan.

Introduced salary exchange to manage

rising employment costs

43%

5.

The UK employeebenefits landscape 5

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Employers who don’t provide healthcare benefits are reliant on an NHS system where employees face huge

challenges in securing timely GP appointments, along with long waits to see specialists and receive treatment.

This all has an impact on sickness absence rates, performance, and ultimately, productivity.

According to the Office of National Statistics, sickness absence rates are at a 15-year high. Helping your people to

understand and improve their physical and emotional health reduces employee stress, improves productivity, and

therefore lowers the costs of sickness absence and presenteeism.

Looking ahead

We asked respondents what their single biggest people/HR priority was for the next 12–24 months. Upskilling (18%),

retention (15%), and reviewing pay and benefits (15%) came out on top. When it comes to upskilling, organisations

are focused on future-proofing talent to prepare for change (including AI tools) and developing leaders. Other

priorities include employee wellbeing, reviewing pensions, and cost-effective reward schemes.

The importance of

understanding your priorities

and challenges

In an uncertain and volatile environment,

it’s more important than ever to carefully

consider your priorities and the risks

associated with achieving your objectives.

Working with an employee benefits specialist

who has a deep understanding of your

objectives as well as the environmental

factors which impact these will make a

huge difference.

Let’s explore smart, sustainable ways to

support your people and your organisation,

for an impact that lasts. Speak with your

Broadstone consultant or get in touch.

We’ve also seen a drop in the number of employers planning to increase their investment in workplace wellbeing.

While this is understandable, given the Budget’s impact, it could be counterproductive. Employers who provide

company-funded healthcare benefits have seen claims and premium costs increase, and minimising claims by

promoting good health is essential to sustainable benefit costs.

6.

The UK employeebenefits landscape 6

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Technology

Benefits technology uses and trends

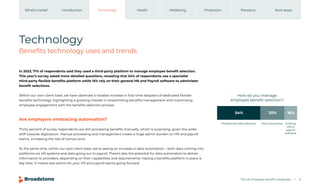

In 2023, 71% of respondents said they used a third-party platform to manage employee benefit selection.

This year’s survey asked more detailed questions, revealing that 54% of respondents use a specialist

third-party flexible benefits platform while 15% rely on their general HR and Payroll software to administer

benefit selections.

Within our own client base, we have observed a notable increase in first-time adopters of dedicated flexible

benefits technology, highlighting a growing interest in streamlining benefits management and maximising

employee engagement with the benefits selection process.

Are employers embracing automation?

Thirty percent of survey respondents are still processing benefits manually, which is surprising, given the wider

shift towards digitisation. Manual processing and management create a huge admin burden on HR and payroll

teams, increasing the risk of human error.

At the same time, within our own client base, we’re seeing an increase in data automation – both data coming into

platforms via HR systems and data going out to payroll. There’s also the potential for data automation to deliver

information to providers, depending on their capabilities and requirements. Having a benefits platform in place is

key here. It means less admin for your HR and payroll teams going forward.

How do you manage

employee benefit selection?

Flexible benefits software Manual process Existing

HR or

payroll

software

54% 30% 16%

7.

The UK employeebenefits landscape 7

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

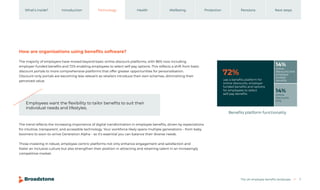

How are organisations using benefits software?

The majority of employers have moved beyond basic online discount platforms, with 86% now including

employer-funded benefits and 72% enabling employees to select self-pay options. This reflects a shift from basic

discount portals to more comprehensive platforms that offer greater opportunities for personalisation.

Discount-only portals are becoming less relevant as retailers introduce their own schemes, diminishing their

perceived value.

The trend reflects the increasing importance of digital transformation in employee benefits, driven by expectations

for intuitive, transparent, and accessible technology. Your workforce likely spans multiple generations – from baby

boomers to soon-to-arrive Generation Alpha – so it’s essential you can balance their diverse needs.

Those investing in robust, employee-centric platforms not only enhance engagement and satisfaction and

foster an inclusive culture but also strengthen their position in attracting and retaining talent in an increasingly

competitive market.

Employees want the flexibility to tailor benefits to suit their

individual needs and lifestyles.

5

Benefits platform functionality

72%

14%

14%

use a benefits platform for

online discounts, employer

funded benefits and options

for employees to select

self-pay benefits

online

discounts and

employer

funded

benefits

online

discounts

only

8.

The UK employeebenefits landscape 8

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

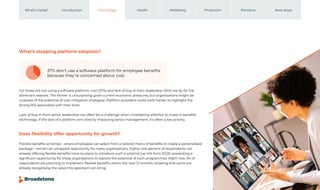

What’s stopping platform adoption?

Does flexibility offer opportunity for growth?

For those still not using a software platform, cost (37%) and lack of buy-in from leadership (34%) are by far the

dominant reasons. The former is unsurprising given current economic pressures, but organisations might be

unaware of the potential of cost mitigation strategies. Platform providers could work harder to highlight the

strong ROI associated with their tools.

Lack of buy-in from senior leadership can often be a challenge when considering whether to invest in benefits

technology. If the lack of a platform isn’t directly impacting senior management, it’s often a low priority.

Flexible benefits schemes – where employees can select from a tailored menu of benefits to create a personalised

package – remain an untapped opportunity for many organisations. Eighty-one percent of respondents not

already offering flexible benefits have no plans to introduce such a scheme (up 14% from 2023), presenting a

significant opportunity for these organisations to explore the potential of such programmes. Right now, 5% of

respondents are planning to implement flexible benefits within the next 12 months, showing that some are

already recognising the value this approach can bring.

37% don’t use a software platform for employee benefits

because they’re concerned about cost.

9.

The UK employeebenefits landscape 9

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Although rising employer costs, such as National Insurance contributions, may be influencing decisions,

this could also be a moment to re-evaluate how the case for flexible benefits is being presented to senior

leaders. Highlighting the advantages of personalisation – where employees can choose benefits that align

with their individual needs and lifestyles – could unlock new engagement and retention opportunities for

forward-thinking organisations.

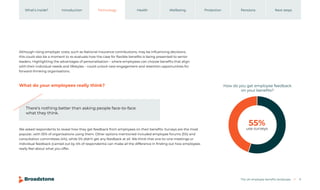

What do your employees really think?

We asked respondents to reveal how they get feedback from employees on their benefits. Surveys are the most

popular, with 55% of organisations using them. Other options mentioned included employee forums (5%) and

consultation committees (4%), while 5% didn’t get any feedback at all. We think that one-to-one meetings or

individual feedback (carried out by 4% of respondents) can make all the difference in finding out how employees

really feel about what you offer.

There’s nothing better than asking people face-to-face

what they think.

How do you get employee feedback

on your benefits?

55%

use surveys

10.

The UK employeebenefits landscape 10

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Health

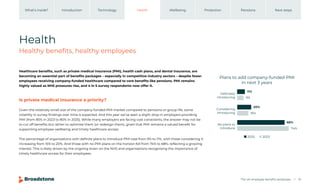

Healthy benefits, healthy employees

Healthcare benefits, such as private medical insurance (PMI), health cash plans, and dental insurance, are

becoming an essential part of benefits packages – especially in competitive industry sectors – despite fewer

employees receiving company-funded healthcare compared to core benefits like pensions. PMI remains

highly valued as NHS pressures rise, and 4 in 5 survey respondents now offer it.

Is private medical insurance a priority?

Given the relatively small size of the company-funded PMI market compared to pensions or group life, some

volatility in survey findings over time is expected. And this year we’ve seen a slight drop in employers providing

PMI (from 85% in 2023 to 80% in 2025). While many employers are facing cost constraints, the answer may not be

to cut off benefits but rather to optimise them (or redesign them), given that PMI remains a valued benefit for

supporting employee wellbeing and timely healthcare access.

The percentage of organisations with definite plans to introduce PMI rose from 9% to 11%, with those considering it

increasing from 15% to 20%. And those with no PMI plans on the horizon fell from 74% to 68%, reflecting a growing

interest. This is likely driven by the ongoing strain on the NHS and organisations recognising the importance of

timely healthcare access for their employees.

Definitely

introducing

Considering

introducing

No plans to

introduce

Plans to add company-funded PMI

in next 3 years

11%

9%

20%

16%

68%

74%

2025 2023

11.

The UK employeebenefits landscape 11

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

How much cover?

Many employers who provide company-funded PMI have seen premiums rise in

recent years, prompting some to consider whether they can afford to continue

funding the benefits. Instead of turning off the tap completely, you could simply

adjust the flow of water by increasing the excess.

The most common excess level remains £100, though it declined overall from 36%

in 2023 to 32%. Meanwhile, a quarter of employers now offer a nil excess plan (2023:

17%), reflecting the fact that many of our respondents operate in sectors where

competition for talent remains fierce. Smaller excess options, such as £50 and £125,

appeared for the first time in the 2025 survey, which indicates a broader variety

is on offer.

More and more employees are struggling to access NHS care, prompting employers

to take a strategic approach and prioritise benefits that maximise wellbeing and

productivity to help mitigate operational risks.

For example, there’s been a shift in the level of benefit provided. Fifty-one percent

of respondents (up from 45% in 2023) offer unlimited outpatient cover, suggesting a

growing preference to offer more comprehensive medical benefits where these are

highly valued by sought-after employees.

40%

35%

30%

25%

20%

15%

10%

5%

0%

2025 2023

£0 £50 £100 £125 £150 £250 £300 £350 £500 £1,000

£200

Level of excess

12.

The UK employeebenefits landscape 12

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

So, what other paid-for health benefits are employers offering?

The proportion of organisations not offering a health cash plan has risen to 65% (2023: 62%), with 25% offering one

to all staff (2023: 24%) and only 9% offering one to a select number of staff (2023: 14%). The health cash plan market

saw growth in 2024, which suggests our findings reflect the particular priorities of our survey participants. Only

4% of respondents have definite plans to introduce a health cash plan in the next three years, and only 26% are

considering introducing one (2023: 41%).

Health cash plans

26% of employers are considering introducing

a health cash plan in the next three years.

Yes to all staff

Yes to selected staff

No

Do you provide a company-funded

health cash plan?

26%

24%

9%

14%

65%

62%

2025 2023

Employers increasingly view PMI as essential for

growth and resilience, not just a discretionary perk.

13.

The UK employeebenefits landscape 13

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

There’s been some growth in the provision of proactive health support: clinic-based screenings rose from 20% in

2023 to 25%, and onsite day screenings from 7% to 10%. But the majority (70%) have no plans to introduce them in

the next three years, suggesting limited momentum towards wider adoption.

Health checks and screenings

Employers not offering dental insurance at all remains high at 76%. This is a slight fall on 2023 (78%), suggesting

a small shift towards broader access. However, only 4% of respondents had definite plans to introduce dental

insurance in the next three years, and the proportion with no plans in the pipeline rose from 68% to 74%.

Dental insurance

Only 17% offer dental insurance to all staff (2023: 14%).

Yes (network of health

screening clinics)

Yes (onsite ‘know your

numbers’ days)

Do you provide company-funded

health checks or screenings?

25%

20%

10%

7%

2025 2023

14.

The UK employeebenefits landscape 14

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Health

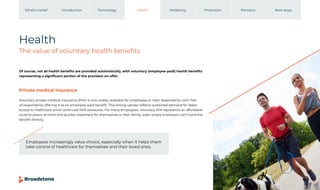

The value of voluntary health benefits

Of course, not all health benefits are provided automatically, with voluntary (employee-paid) health benefits

representing a significant portion of the provision on offer.

Voluntary private medical insurance (PMI) is now widely available for employees or their dependants, with 74%

of respondents offering it as an employee-paid benefit. This strong uptake reflects sustained demand for faster

access to healthcare amid continued NHS pressures. For many employees, voluntary PMI represents an affordable

route to peace of mind and quicker treatment for themselves or their family, even where employers can’t fund the

benefit directly.

Private medical insurance

Employees increasingly value choice, especially when it helps them

take control of healthcare for themselves and their loved ones.

15.

The UK employeebenefits landscape 15

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Over half of respondents (57%) provide voluntary dental insurance, suggesting that access to routine and

preventative care remains a priority in the face of declining access to NHS dental services. This approach allows

employees to manage everyday healthcare needs flexibly, while keeping employer costs in check.

Voluntary health screening is offered by 68% of respondents, underlining a growing commitment to preventative

wellbeing. Even without company funding, many organisations recognise the importance of giving employees

access to health assessments that can detect issues early and encourage them to adopt healthier lifestyles.

And the costs of voluntary health screenings are often discounted by providers to encourage greater take

up by employees.

Together, these findings highlight a clear trend: employers are expanding voluntary options to meet employee

expectations for accessible, personalised healthcare. Employee-paid options allow employers to support their

staff’s health while maintaining financial sustainability. They also help employees access the benefits that are most

relevant to them and their families.

Dental insurance

Health checks and screenings

11

Health

checks

68% 27%

5%

Do you offer voluntary

(employee paid) health benefits?

Dental 57% 37%

6%

Private

medical

74% 21%

5%

Offer now No plans to offer

Plan to offer in next 3 years

16.

The UK employeebenefits landscape 16

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

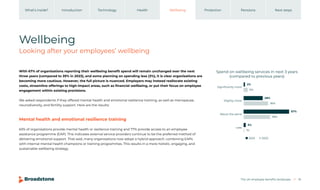

Wellbeing

Looking after your employees’ wellbeing

Mental health and emotional resilience training

63% of organisations provide mental health or resilience training and 77% provide access to an employee

assistance programme (EAP). This indicates external service providers continue to be the preferred method of

delivering emotional support. That said, many organisations now adopt a hybrid approach, combining EAPs

with internal mental health champions or training programmes. This results in a more holistic, engaging, and

sustainable wellbeing strategy.

With 67% of organisations reporting their wellbeing benefit spend will remain unchanged over the next

three years (compared to 39% in 2023), and some planning on spending less (3%), it is clear organisations are

becoming more cautious. However, the full picture is nuanced. Employers may instead reallocate existing

costs, streamline offerings to high-impact areas, such as financial wellbeing, or put their focus on employee

engagement within existing provisions.

We asked respondents if they offered mental health and emotional resilience training, as well as menopause,

neurodiversity, and fertility support. Here are the results:

Significantly more

Slightly more

About the same

Spend on wellbeing services in next 3 years

(compared to previous years)

2%

6%

28%

36%

67%

39%

Less

3%

1%

2025 2023

17.

The UK employeebenefits landscape 17

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

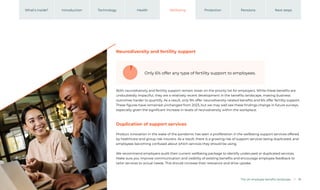

Menopause support is shifting from

signposting to company-funded.

Menopause support

Menopause support has seen the largest shift from

being an externally signposted solution to a company-

funded benefit, with 20% of organisations now

offering it. This is likely driven by demographics and

high profile public campaigns, creating a greater

awareness. This type of support can include flexible

working and workplace adjustments as well as access

to specific healthcare solutions or ancillary services

within existing insured arrangements.

Fertility 6% 14%

Wellbeing support

Gender

dysphoria

3% 11%

Menopause 20% 19%

Neurodiversity 9% 16%

Yes, company funded support

Yes, signposted to external

service provider

18.

The UK employeebenefits landscape 18

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Both neurodiversity and fertility support remain lower on the priority list for employers. While these benefits are

undoubtedly impactful, they are a relatively recent development in the benefits landscape, making business

outcomes harder to quantify. As a result, only 9% offer neurodiversity-related benefits and 6% offer fertility support.

These figures have remained unchanged from 2023, but we may well see these findings change in future surveys,

especially given the significant increase in levels of neurodiversity within the workplace.

Duplication of support services

Product innovation in the wake of the pandemic has seen a proliferation in the wellbeing support services offered

by healthcare and group risk insurers. As a result, there is a growing risk of support services being duplicated, and

employees becoming confused about which services they should be using.

We recommend employers audit their current wellbeing package to identify underused or duplicated services.

Make sure you improve communication and visibility of existing benefits and encourage employee feedback to

tailor services to actual needs. This should increase their relevance and drive uptake.

Neurodiversity and fertility support

Only 6% offer any type of fertility support to employees.

19.

The UK employeebenefits landscape 19

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Wellbeing

Supporting your employees’ financial wellbeing

How important is financial wellbeing?

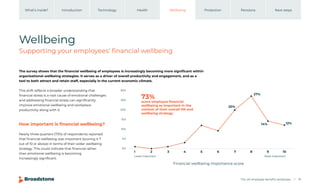

Nearly three quarters (73%) of respondents reported

that financial wellbeing was important (scoring it 7

out of 10 or above) in terms of their wider wellbeing

strategy. This could indicate that financial rather

than emotional wellbeing is becoming

increasingly significant.

The survey shows that the financial wellbeing of employees is increasingly becoming more significant within

organisational wellbeing strategies. It serves as a driver of overall productivity and engagement, and as a

tool to both attract and retain staff, especially in the current economic climate.

This shift reflects a broader understanding that

financial stress is a root cause of emotional challenges

and addressing financial stress can significantly

improve emotional wellbeing and workplace

productivity along with it.

30%

25%

20%

15%

10%

5%

0%

1 2 3 4 5 6 7

27%

14% 12%

20%

8 9 10

Financial wellbeing importance score

Most important

Least important

73%

score employee financial

wellbeing as important in the

context of their overall HR and

wellbeing strategy

20.

The UK employeebenefits landscape 20

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pathways to support financial wellbeing

The road ahead

But what about the ways organisations support their employees’ financial wellbeing? Although respondents

recognise its importance, there’s been a decline in what they offer since our 2023 survey. That includes one-to-one

meetings, webinars, online calculators, and other online tools. This decrease might be due to organisations relying

more heavily on existing solutions with external service providers, such as employee assistance programmes, due

to budget constraints.

Although many organisations clearly see financial wellbeing solutions as an important part of their wider

wellbeing strategy, implementation is lagging. The gap between intention and access means employees may

continue to struggle with financial stress, which in turn can affect their emotional wellbeing.

Employers should adopt cost-efficient but high-value solutions, such as digital platforms for scalable support,

flexible on-demand services, and group-wide initiatives, such as workshops and webinars.

Webinars, used by 48% of organisations, are the most popular

way employers support employees’ financial wellbeing.

Personal financial planning

services for your people

Every employee deserves to know their

financial future is in safe hands. But

whether they’re just starting out, growing

their savings, or planning for retirement,

navigating today’s financial landscape can

feel overwhelming.

That’s why we offer expert, personalised

advice, from one-off consultations to ongoing

support. We take the time to understand

an individual’s circumstances, goals, and

priorities, and then create an actionable plan

that evolves with their needs.

Providing your employees with access to the

right financial planning support (whether

company-funded or employee-paid) isn’t

just good for them – it’s good for your

organisation. Financial wellbeing boosts

morale, productivity, and retention. It shows

your people that you care, and that you’re

invested in their future.

21.

The UK employeebenefits landscape 21

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Protection

Protecting them for life

Our survey asked respondents all about their protection benefits, including group life assurance, group

income protection, and critical illness cover. Across all three, provision levels have remained broadly stable

since 2023, reflecting a continued recognition of their value in employee benefits strategies.

Almost universal protection

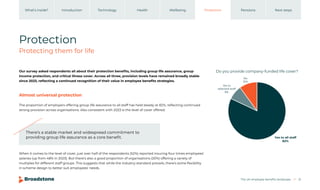

The proportion of employers offering group life assurance to all staff has held steady at 82%, reflecting continued

strong provision across organisations. Also consistent with 2023 is the level of cover offered.

When it comes to the level of cover, just over half of the respondents (52%) reported insuring four times employees’

salaries (up from 48% in 2023). But there’s also a good proportion of organisations (20%) offering a variety of

multiples for different staff groups. This suggests that while the industry-standard prevails, there’s some flexibility

in scheme design to better suit employees’ needs.

There’s a stable market and widespread commitment to

providing group life assurance as a core benefit.

Do you provide company-funded life cover?

Yes to all staff

82%

No

10%

Yes to

selected staff

8%

22.

The UK employeebenefits landscape 22

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Finding flexibility in group life assurance

With only 9% of employers currently offering flexible group life assurance cover, there’s a clear opportunity to

better support employees, especially those with significant financial or family responsibilities, by giving them more

choice in how their cover is structured.

Seventy-nine percent of organisations are currently offering voluntary life cover to employees (2023: 55%), with

33% also extending the offer to spouses and partners (2023: 16%), both significant increases since 2023.

We’ve also seen a slight increase in the share of employers now offering excepted life schemes (instead of, or

alongside, a registered life scheme), which stands at 33% (2023: 30%). This highlights the fact that excepted life

schemes have become an important and established part of the wider employee benefits strategy.

Group life assurance’s stability highlights its importance as a core protection benefit. But employers need

to make sure they regularly review the benefit’s structure, including the question of registered versus

excepted cover options, and think about how this type of protection can be positioned within a broader

flexible benefits framework.

Offering salary exchange options can increase engagement

and perceived value without significant cost increases.

23.

The UK employeebenefits landscape 23

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Protection

Protecting the future for families

The proportion of employers offering group income protection remains steady at 47%, with the same

number of respondents offering it to all staff (32%) and a select group of staff (15%) as in 2023. A 26-week

deferment period remains the most common approach, as in previous years, and was reported by almost

three quarters of respondents.

While overall provision has not significantly changed, ongoing developments in insurer-led intervention and

rehabilitation support, together with wellbeing services, highlight the continued importance of this benefit. For

alignment and cost-effectiveness, you should review how group income protection integrates with your sick-pay

policies, absence processes, and wellbeing strategy.

What’s covered?

As with our 2023 results, the most common level of income protection benefit is 75% of employees’ salaries (41%

of organisations offer this). While 50% is the second most popular choice (28% of respondents). This demonstrates

there’s some variation in plan design as employers balance cost considerations, wellbeing support, and workforce

expectation with the level of benefit provided

100% of salary

95% of salary

80% of salary

75% of salary

70% of salary

65% of salary

60% of salary

50% of salary

15% of salary

3%

1%

3%

41%

4%

10%

1%

7%

28%

What percentage of salary is insured?

.

24.

The UK employeebenefits landscape 24

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Salary exchange options

Popular payment terms

The number of employers offering salary exchange options for group income protection remains low at just 4%

(as per 2023). This reflects the complications around double taxation of employees who receive a payment from

the policy in relation to sickness or disability. Unfortunately, this continues to be a key industry issue and is holding

back wider policy growth and adoption.

Nearly half of respondents continue to insure benefits to State Pension age although this has reduced slightly

from 2023 (48% to 46%). However, we’re also seeing a rise in limited payment terms, such as two or three years. This

evolution of plan designs is likely caused by employees being less likely to stay at one organisation for their whole

career and employers seeking to manage costs while maintaining cover.

Limited payment terms reflect a workforce that’s less

likely to remain with one employer.

25.

The UK employeebenefits landscape 25

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Protection

Protecting employees when sickness strikes

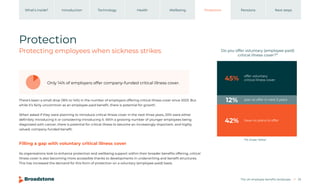

There’s been a small drop (16% to 14%) in the number of employers offering critical illness cover since 2023. But

while it’s fairly uncommon as an employee-paid benefit, there is potential for growth.

When asked if they were planning to introduce critical illness cover in the next three years, 20% were either

definitely introducing it or considering introducing it. With a growing number of younger employees being

diagnosed with cancer, there is potential for critical illness to become an increasingly important, and highly

valued, company-funded benefit.

Only 14% of employers offer company-funded critical illness cover.

Filling a gap with voluntary critical illness cover

As organisations look to enhance protection and wellbeing support within their broader benefits offering, critical

illness cover is also becoming more accessible thanks to developments in underwriting and benefit structures.

This has increased the demand for this form of protection on a voluntary (employee-paid) basis.

Do you offer voluntary (employee paid)

critical illness cover?*

have no plans to offer

plan to offer in next 3 years

offer voluntary

critical illness cover

12%

45%

42%

*1% chose ‘Other’

26.

The UK employeebenefits landscape 26

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Currently, 45% of respondents said they currently offer critical illness as a voluntary benefit and 12% said they

planned to put a voluntary option in place for employees in the next three years. This will help fill an important gap

in employees’ financial protection at a relatively low cost to employers.

Voluntary critical illness cover enhances the benefits choice on offer. And because it’s simple to integrate into

existing platforms, it requires minimal administration too.

Developments in underwriting and benefit structure have

made critical illness cover more accessible than ever before.

27.

The UK employeebenefits landscape 27

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pensions

What type of pension scheme are you providing?

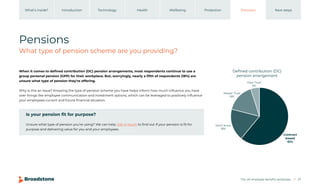

When it comes to defined contribution (DC) pension arrangements, most respondents continue to use a

group personal pension (GPP) for their workplace. But, worryingly, nearly a fifth of respondents (18%) are

unsure what type of pension they’re offering.

Why is this an issue? Knowing the type of pension scheme you have helps inform how much influence you have

over things like employee communication and investment options, which can be leveraged to positively influence

your employees current and future financial situation.

Is your pension fit for purpose?

Unsure what type of pension you’re using? We can help. Get in touch to find out if your pension is fit for

purpose and delivering value for you and your employees.

Defined contribution (DC)

pension arrangement

Contract

based

61%

Own Trust

5%

Master Trust

16%

Don’t know

18%

28.

The UK employeebenefits landscape 28

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Why do you provide a pension?

While 31% of respondents are primarily offering a DC pension to comply with automatic enrolment requirements

(2023: 28%), it’s encouraging to see a slight increase in employers focused on a different purpose. Thirty-five

percent (up from 32% in 2023) said the main reason for their DC pension offering was ensuring employees have

adequate retirement savings.

As shortfalls in retirement income remain a serious risk, it’s worth considering how visible your pension is to

employees. And while it might be part of your competitive recruitment and retention strategy, like 34% of

respondents, this essential benefit is also a sign of your organisational values, priorities, and commitment to

staff wellbeing.

Main purpose of your pension

34% part of

competitive

recruitment

and retention

strategy

31% compliance

with auto-enrolment

35% ensuring employees

have adequate retirement savings

29.

The UK employeebenefits landscape 29

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pensions

Contributing to your employees’ pension pots

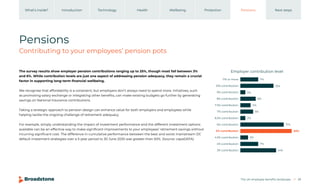

The survey results show employer pension contributions ranging up to 25%, though most fall between 3%

and 6%. While contribution levels are just one aspect of addressing pension adequacy, they remain a crucial

factor in supporting long-term financial wellbeing.

We recognise that affordability is a constraint, but employers don’t always need to spend more. Initiatives, such

as promoting salary exchange or integrating other benefits, can make existing budgets go further by generating

savings on National Insurance contributions.

Taking a strategic approach to pension design can enhance value for both employers and employees while

helping tackle the ongoing challenge of retirement adequacy.

For example, simply understanding the impact of investment performance and the different investment options

available can be an effective way to make significant improvements to your employees’ retirement savings without

incurring significant cost. The difference in cumulative performance between the best and worst mainstream DC

default investment strategies over a 5-year period to 30 June 2025 was greater than 50%. (Source: capaDATA).

11% or more

10% contribution

9% contribution

8% contribution

7.5% contribution

7% contribution

6.5% contribution

6% contribution

5% contribution

4.5% contribution

4% contribution

3% contribution

7%

20%

2%

13%

6%

4%

5%

2%

17%

14%

3%

7%

Employer contribution level

30.

The UK employeebenefits landscape 30

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

What do employees have to put in?

Who’s opting out?

Almost a third (30%) of employers set the minimum employee pension contribution at 5%, consistent with 2023

findings and reflecting the continued use of the auto-enrolment minimum. However, the minimum level of

contributions risk leaving employees short of a comfortable retirement income. One way employers can help

address this is through financial education, which enables staff to budget effectively and plan for the future

with confidence.

Around 15% of employers reported that at least 2% of their workforce have reduced or opted out of pension

contributions in the past year. This trend highlights growing affordability pressures and low financial confidence

among employees.

These choices may be driven by anxiety or financial stress, potentially affecting wellbeing and absenteeism –

perhaps you’re already noticing this with some employees? Financial education and active pension oversight

can help identify early warning signs and support better decision-making. With tailored programmes to suit all

budgets, employers can play a crucial role in improving the financial resilience of their employees.

8% contribution

6% contribution

5% contribution

4.5% contribution

4% contribution

3% contribution

2% contribution

1% contribution

0% contribution

1%

9%

30%

2%

4%

23%

25%

2%

5%

Minimum employee contribution

31.

The UK employeebenefits landscape 31

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pensions

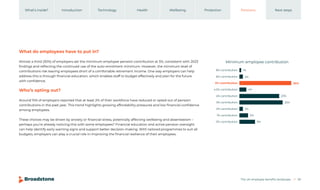

How salary exchange for pensions is a win-win

The percentage of organisations using salary exchange (also known as salary sacrifice) for pensions has risen

from 77% in 2023 to 83% this year. This will not come as a surprise, considering the increases in employers’

National Insurance (NI) from April 2025.

However, this still leaves 17% of our survey respondents who are potentially missing out on a highly effective way

to mitigate these increased costs. This could be because of a lack of awareness or knowledge gaps around the

benefits of using salary exchange.

Pension salary exchange remains one of the most effective ways to make contributions more affordable for both

employees and employers, delivering valuable NI savings while supporting better long-term financial outcomes.

With potential reforms to salary exchange schemes expected in the Autumn Budget 2025, it’s something we’re

keeping a close eye on.

Get started with pension salary exchange

Implementing a salary exchange arrangement for your pension scheme requires careful assessment,

planning and clear communication. That’s something our expert consultants can help you with, making

sure you’re compliant and maximising the benefits for you and your employees.

Yes

No

Don’t know

Do you use pension salary exchange?

83%

77%

15%

21%

2%

2%

2025 2023

32.

The UK employeebenefits landscape 32

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Putting employees’ financial futures first

Of those employers where salary exchange for pensions is available, nearly a third (32%) share the employer NI

savings with their employees – half of which share 100% of the savings made. Aside from the 3% who responded

‘don’t know’, the majority have other ideas. We’ve seen an increase in the percentage of employers not sharing NI

savings up from 56% in 2023 to 65%.

This is not unexpected either. Employers are being forced to make difficult decisions because of the Government’s

changes to NI and National Living Wage and National Minimum Wage rates. Unfortunately, this has the potential

to negatively impact outcomes for employees’ retirement as a result.

9% increase in the number of employers

not sharing NI savings with employees.

33.

The UK employeebenefits landscape 33

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pensions

Supporting your employees to understand pensions

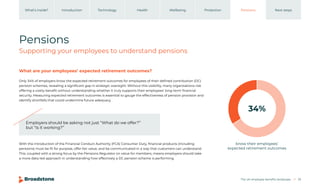

What are your employees’ expected retirement outcomes?

Only 34% of employers know the expected retirement outcomes for employees of their defined contribution (DC)

pension schemes, revealing a significant gap in strategic oversight. Without this visibility, many organisations risk

offering a costly benefit without understanding whether it truly supports their employees’ long-term financial

security. Measuring expected retirement outcomes is essential to gauge the effectiveness of pension provision and

identify shortfalls that could undermine future adequacy.

With the introduction of the Financial Conduct Authority (FCA) Consumer Duty, financial products (including

pensions) must be fit for purpose, offer fair value, and be communicated in a way that customers can understand.

This, coupled with a strong focus by the Pensions Regulator on value for members, means employers should take

a more data-led approach in understanding how effectively a DC pension scheme is performing.

Employers should be asking not just “What do we offer?”

but “Is it working?”

know their employees’

expected retirement outcomes

34%

23

34.

The UK employeebenefits landscape 34

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Those with insight into their employees’ expected outcomes are better positioned to make informed changes,

which improve retirement outcomes and demonstrate tangible value. This ensures pensions remain both a vital

employee benefit and a driver of long-term financial security.

When it comes to the guidance and support on offer to employees, the results reflect a growing recognition of

the importance of financial education and retirement planning. Webinars remain the most common form of

guidance, providing accessible, cost-effective engagement for diverse workforces. However, we believe one-to-

one sessions, and where appropriate financial advice, can deliver the greatest impact, particularly for employees

nearing retirement.

This shift towards more proactive engagement shows that employers increasingly understand the link between

financial wellbeing, retention, and productivity. Yet, the 14% still offering no guidance risk leaving employees ill-

equipped to plan effectively for retirement. Working with an expert consultancy like Broadstone can help you

design scalable employee support that builds financial confidence, improves outcomes, and strengthens trust.

How are employers helping?

The proportion of employers offering no support to employees in

relation to pensions and retirement has fallen from 24% to 14%.

One-to-one

support

Online

calculators

Other

online tools

Retirement planning support

offered to employees

21%

33%

21%

24%

24%

31%

None

14%

24%

Webinars

38%

43%

2025 2023

35.

The UK employeebenefits landscape 35

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Pensions

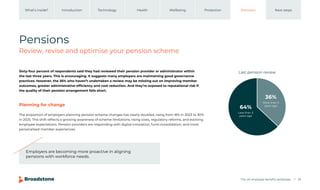

Review, revise and optimise your pension scheme

Sixty-four percent of respondents said they had reviewed their pension provider or administrator within

the last three years. This is encouraging. It suggests many employers are maintaining good governance

practices. However, the 36% who haven’t undertaken a review may be missing out on improving member

outcomes, greater administrative efficiency and cost reduction. And they’re exposed to reputational risk if

the quality of their pension arrangement falls short.

The proportion of employers planning pension scheme changes has nearly doubled, rising from 16% in 2023 to 30%

in 2025. This shift reflects a growing awareness of scheme limitations, rising costs, regulatory reforms, and evolving

employee expectations. Pension providers are responding with digital innovation, fund consolidation, and more

personalised member experiences.

Planning for change

Employers are becoming more proactive in aligning

pensions with workforce needs.

Last pension review

More than 3

years ago

Less than 3

years ago

36%

64%

36.

The UK employeebenefits landscape 36

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

The drivers for change

Cost remains the primary motivator for reviewing pension schemes, with 6% of employers citing rising

administration, platform, and investment fees. They’re focused on achieving better value for money and ensuring

strong employee outcomes.

A further 3% cited regulatory compliance, likely linked to upcoming Mansion House reforms, while 11% referenced

“other” reasons, such as poor provider service; environmental, social and governance (ESG) integration; digital

engagement; or better default fund performance. These responses suggest a growing focus on strategic

alignment to make sure pensions meet both organisational and employee goals.

With the Mansion House reforms driving consolidation, scale, and increased UK investment, employers need to

assess whether their current provider is aligned with future expectations. Consider scheduling a provider review

every three years and benchmarking against market standards, including ESG credentials, digital capabilities,

member engagement tools, and legislation.

If service levels or digital engagement are lacking, consider alternative providers that better align with your

strategic goals. And don’t forget to refresh training materials and governance frameworks to reflect current

standards and new initiatives.

Employers are committed to supporting retirement savings –

only 3% of respondents are considering reducing contributions.

37.

Introduction Technology HealthWellbeing Protection Pensions

What’s inside? Next steps

Next steps

Want to know more?

Our 2025 survey and analysis highlight key shifts in employer priorities.

We’ve seen organisations leveraging technology thoughtfully to streamline administration and promote inclusivity

through tailored messaging. Employee communication continues to be a challenge for stretched HR teams,

who are also tackling the issues posed by increasing economic pressures, such as the rise in employer National

Insurance contributions.

In healthcare, the value of private medical cover is being realised, particularly as NHS pressures continue to rise.

And there’s been an expansion of added-value benefit options to meet employee expectations. While across

employee protection benefits – group life assurance, group income protection, and critical illness cover – we’re

seeing continued stability in the main.

There’s been a rise in the number of employers using salary exchange for pensions, but employers have limited

knowledge of the expected retirement outcomes of their people. That said, there is a growing awareness of

pension scheme limitations, rising costs, regulatory reforms, and evolving employee expectations.

However, even with technological innovation, strategic benefit reviews, and a growing focus on wellbeing,

many organisations still struggle to balance affordability, effectiveness, and employee expectations.

That’s where we come in.

38.

The UK employeebenefits landscape 38

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Expertise and experience

Strategic and flexible

With over 40 years’ experience, we know the employee benefits landscape inside-out. As a people-first

consultancy, we bring clarity, independence, and insight to every stage of your benefits provision – from design

and provider assessment to implementation and communication.

We’ll consider your strategy and priorities over the short and medium term, help you review your current

approach, identify efficiencies, and ensure your benefits deliver real impact and value for money. And we take an

agile approach, anticipating and responding to your needs, regardless of your size or resources.

We turn complex benefit decisions into confident

strategies that work for your people and your organisation.

Benefits that work — for you and your people

At Broadstone, we believe employee benefits should do more than tick boxes — they should drive engagement,

retention, and wellbeing while aligning with your organisational goals, culture and values. Our approach helps you

deliver benefits that are bold, brilliant, and built for your people’s changing needs.

39.

The UK employeebenefits landscape 39

Introduction Technology Health Wellbeing Protection Pensions

What’s inside? Next steps

Thanks to our contributors

We’d like to thank the 200 organisations who took part in this survey – without them, we wouldn’t have this report.

To mark their contribution, we’ve donated £2,000 to Macmillan Cancer Support (£10 for every completed survey).

And thank you to our consultants whose expertise was key in delivering this report:

Benefits technology

Ruth Empson-Ridge

Andrew Mobberley

Craig Williams

Health

James Lang

Wellbeing

Jamie Burdess

Kelly Parsons

Protection

Richard Pringle

Pensions

Jeremy Brown

Matt Dorrington

Chloe Griffiths

Kelly Parsons

Ian Roylance

40.

The UK employeebenefits landscape (November 2025) 40

Broadstone is a trademark owned by Broadstone Corporate Benefits Limited and used by companies in the Broadstone group.

Broadstone Financial Solutions Limited is authorised and regulated by the Financial Conduct Authority.

Registered in England and Wales under no. 02131269. Registered office 100 Wood Street, London EC2V 7AN.

EBSURVEY NOV25

Discover how our consultants can help you

create an employee benefits strategy that

truly makes an impact – for your organisation

and your people.

Contact us

broadstone.co.uk/employee-benefits-wellbeing/

corporate@broadstone.co.uk