A monthly subscription newsletter from DieselNet. See endnotes for information on subscription and copyrights.ISSN 1718-3537

Downloaded by Guest

Regulatory Trends

Germany relaunches EV subsidy program

Germany is re-introducing a subsidy scheme for buying electric vehicles with federal funds. The new EV incentive program, with a budget of 3 billion EUR by 2029, takes effect retroactively from 1 January 2026.

The previous EV incentive program was discontinued at the end of 2023 due to budget constraints. The end of the incentive program resulted in a plunge in German EV sales in the following months.

Details on the new program have been published by the German Ministry for the Environment, Climate Protection, Nature Conservation, and Nuclear Safety (BMUKN).

The new subsidy scheme is applicable to new class M1 vehicles with battery-electric drive (BEV), as well as to range extended electric vehicles (REEV) and plug-in hybrid electric vehicles (PHEV). PHEVs and REEVs must have a minimum electric range of 80 km and maximum CO2 emissions of 60 g/km to be eligible.

The total fund of 3 billion EUR is expected to last for 800,000 applications. The program is limited to the private sector. Vehicles must be kept (purchased or leased) for a period of at least 36 months.

Eligible applicants must have a maximum taxable income of 80,000 EUR per household, which can be increased to 90,000 EUR for families with children.

The incentives for BEVs range from 3,000 to 6,000 EUR per vehicle, depending on the household income and the number of children. Subsidies for PHEV and REEV vehicles range from 1,500 to 4,500 EUR. Online applications can start in May for vehicles registered from 1 January 2026.

The subsidies are applicable to all EVs, including vehicles imported from China or other countries. The program does not require mandatory discounts by OEMs.

WGMM critical about the EU Commission’s proposal for revised CO2 standards

The Working Group on Monitoring Methodologies for CO2 neutral fuels

(WGMM)—a group of over 50 European automotive and fuel suppliers—issued a statement critical of the European Commission’s new proposal within the Automotive Package to revise the CO2 emission standards for light-duty vehicles.

The Commission’s new proposal is an important recognition of the importance of renewable fuels, specifically e-Fuels and biofuels, as contributors to road transport decarbonization, stated the WGMM. Regrettably, the proposal does not go far enough in unleashing the potential of those fuels to help deliver on EU goals for reducing emissions.

legislation that recognizes all verifiable, RED-compliant sustainable fuels and adopts a single, harmonized definition of such fuels; and

the approval of a new vehicle class operating exclusively on certified CO2 neutral fuels as compliant with future emission standards.

The WGMM therefore strongly regrets that the Commission has not followed through on its commitment under recital 11 of Regulation (EU) 2023/851 in the new Automotive Package proposal on revised CO2 standards. That recital explicitly required the Commission to present a proposal allowing the registration, after 2035, of vehicles running exclusively on CO2-neutral fuels. By omitting this commitment, the proposal weakens the long-term regulatory signal for CO2-neutral fuels and overlooks the robust monitoring framework developed by the WGMM.

On January 1st, the EU carbon border adjustment mechanism (CBAM) entered into effect. The CBAM works alongside the EU Emissions Trading System to prevent carbon leakage by imposing carbon pricing on imports.

Under the world’s first carbon border tax mechanism, importers of carbon-intensive goods into the EU from six covered sectors—aluminum, cement, electricity, fertilizers, iron and steel, and hydrogen—will now be required to purchase CBAM certificates corresponding to the embedded carbon content of their products.

This marks the end of a transitional reporting-only period that began in October 2023, ushering in what industry experts describe as the world’s most radical carbon pricing policy, with far-reaching implications for global commodity trade flows.

The run-up to CBAM’s definitive phase has been anything but smooth. The European Commission provided key details—including default values, CBAM benchmarks, and emission calculation methodologies—only in mid-December, leaving importers worldwide ill-prepared and anxious.

Importers can purchase CBAM certificates starting February 2027 to cover emissions from their 2026 imports, providing businesses time to adapt to the carbon pricing mechanism. Importers also have until September 2027 to submit their first CBAM declarations for 2026 imports.

However, while companies awaited clarity on CBAM benchmarks and default values, the price of carbon, which forms the basis of CBAM certificates, underwent significant changes, particularly toward the end of 2025—European carbon prices surged to multi-year highs in December as the supply of allowances tightened due to reduced auction volumes.

EU Allowances averaged €84.95/mt in December, the highest monthly average since August 2023, and up 25% compared with December 2024, according to data from Platts.

Reactions to CBAM have been wide-ranging, with many developing and emerging economies expressing frustration over what they view as trade protectionism. The EU’s carbon border levy is “unfair” and “discriminatory,” China’s Ministry of Commerce said in a statement, vowing to take countermeasures to defend the country’s interests.

The CBAM carbon tariff has also been criticized by India, the world’s second-largest steel producer after China and a major steel exporter to the European Union.

US DOJ will no longer pursue criminal charges for motor vehicle emission tampering

The US Department of Justice (DOJ) Environment and Natural Resources Division announced in a post on X that the DOJ will no longer pursue criminal charges under the Clean Air Act (CAA) related to tampering with onboard diagnostic devices in motor vehicles.

The DOJ said it is exercising its “enforcement discretion”. The agency has not provided reasons for the decision.

Emission tampering involves changes in hardware or software in in-use vehicles that impair the vehicle’s emission control system. Common examples include the installation of electronic “tuners” that reprogram the vehicle’s original software or “DPF delete” kits that allow the removal of particulate filters from diesel vehicles.

The DOJ will still “pursue civil enforcement for these violations when appropriate,” the agency said in their X post.

In 2020, the Environmental Protection Agency started the National Compliance Initiative (NCI) that pursued, in cooperation with the DOJ, emission violation enforcement in existing, in-use vehicles. Under the NCI program, the agency fined a number of suppliers and installers of tampering devices and software—referred to as illegal emission defeat devices. While most of the enforcement involved out of court settlements, some cases involved criminal penalties.

According to the EPA, under the NCI initiative, the agency finalized 172 civil enforcement cases from FY 2020 through FY 2023 resulting in civil penalties totaling $55.5 million. During the same period, the EPA completed 17 criminal cases resulting in penalties totaling $5.6 million, $1.2 million in restitution, $438,000 in environmental projects, and 54 months of incarceration.

However, the EPA web page does not provide details on enforcement activities during 2024 and 2025. In November 2025, a Wyoming diesel tuner who was imprisoned after being convicted on hundreds of counts of violating EPA emission regulations received an unconditional pardon from President Trump.

UK opens consultation on HGV CO2 emissions regulatory framework

The UK Department for Transport (DfT) opened a consultation committing to the phase-out of non-zero emission heavy-goods vehicles (HGV) by 2035 for trucks up to 26 tonnes and 2040 for all trucks. The DfT is seeking input on a future CO2 emissions regulation for the road freight sector.

The consultation is divided into five sections:

Part A provides a background on the current HGV market in the UK and seeks input on whether the certification regulation (i.e., the regulation behind VECTO) in the UK should be aligned with the EU.

Part B considers potential regulatory options, whether a CO2 standard, ZEV mandate, or fleet mandate should be employed.

Part C considers scope and eligibility criteria for “zero emission”. It rules out low-carbon fuels, but is open to how H2 combustion should be dealt with. It also asks whether coaches and trailers should be included in the scope of this regulation.

Part D seeks views options on the categorization of vehicles, flexibilities, and penalties. It proposes to maintain the VECTO grouping, and assigns each VECTO group into the 2035 or 2040 phase-out date.

Part E seeks input on CO2 emissions reduction trajectories for a future regulatory framework.

While the EU has weakened the stringency of its CO2 standards for new vehicles, the UK seems to be going the opposite direction by supporting the transition to zero emission heavy goods vehicles.

Australia publishes new draft standard for CO2 emission measurement

Australia has published a draft new Vehicle Standard (Australian Design Rule) ADR 114/00 – Carbon Dioxide Emissions Measurement. The standard will regulate CO2 emissions testing requirements for specified vehicles with a gross vehicle mass (GVM or maximum laden vehicle mass) between 3,500 kg and 3,855 kg from 1 January 2027. This proposed rulemaking will align Australia’s CO2 testing requirements with equivalent US standards for light duty vehicles, which apply to vehicles with a gross vehicle weight rating up to 8,500 lbs.

This new vehicle standard is proposed as an initial step to enable vehicles with a GVM up to 4,500 kg that are marketed to be driven by consumers (such as full-sized sport utility vehicles and pick-ups) to be subject to the requirements of the New Vehicle Efficiency Standard Act 2024 (NVES Act). This was foreshadowed by the Australian Government in the ‘Cleaner, Cheaper to Run Cars: The Australian New Vehicle Efficiency Standard’ Impact Analysis’, which was notified in March 2024.

The NVES Act sets sales weighted average CO2 emissions targets for vehicle manufacturers supplying vehicles covered by the NVES Act with a GVM rating up to 4,500 kg to Australia from 2025. The NVES Act commenced on 1 January 2025, with assessment of compliance commencing for all NVES Act covered vehicles supplied from 1 July 2025.

The NVES Act uses the CO2 numbers entered for each covered vehicle on the Australian Government’s Register of Approved Vehicles (RAV) to determine whether a manufacturer complies with the NVES. The CO2 emissions number reported on the RAV is determined in accordance with the relevant Australian Design Rule for measuring CO2 emissions.

The Australian Government adopted the New Vehicle Efficiency Standard Determination 2024 on 27 November 2024 to exempt vehicles that do not have a CO2 test procedure mandated by an ADR (such as vehicles with a GVM above 3,500 kg) from assessment of compliance under the NVES Act, until the calendar year after a CO2 emissions test has been mandated by an ADR.

Now that an appropriate test has been identified, the Australian Government proposes that vehicles with a GVM over 3,500 kg and less than 3,855 kg be required to obtain a CO2 emissions test from 1 January 2027. A further rulemaking is proposed to amend the New Vehicle Efficiency Standard Determination 2024 to include these vehicles in the NVES framework from 1 July 2027.

The proposed standard adopts a conversion procedure to enable vehicles tested to WLTP or US test procedures to comply with the NVES Act.

Brazil sets new emission reduction targets for fuels

Brazil’s National Council for Energy Policy (CNPE) published a resolution fixing annual mandatory targets to reduce GHG emissions from fuel sales for the period between 2026 and 2035. The move reinforces RenovaBio, the country’s National Biofuels Policy.

Under the resolution, the fuel sector will follow a defined decarbonization path over the next decade, with the carbon intensity of the fuel mix expected to fall by 11.8% by 2035 compared with 2018 levels. The targets were drawn up based on a Regulatory Impact Analysis prepared by the Ministry of Mines and Energy.

Since its launch, RenovaBio has played a significant role in lowering emissions from Brazil’s transport sector by encouraging greater use of ethanol, biodiesel and biomethane.

California sunsets biodiesel NOx emission mitigation requirements

The California Air Resources Board (CARB) has ended the NOx emission mitigation requirement for biodiesel blends up to B20 (20% biodiesel) in the Alternative Diesel Fuel (ADF) regulation.

Biodiesel blends can increase NOx emissions from diesel engines. To mitigate these increased NOx emissions, the CARB ADF regulation required producers to mix a minimum of 55% renewable diesel with biodiesel in blends from B6 to B20 intended for on-road engines.

The ADF NOx mitigation requirements were designed for older technology engines, without NOx reduction catalysts. In modern engines, the increased NOx levels that may be caused by the use of biodiesel are reduced over the SCR catalyst. The ADF regulation included a sunset clause to the effect that when the vehicle miles traveled (VMT) by new technology diesel engines reaches 90% of the overall VMT by the California heavy-duty vehicle fleet, the biodiesel NOx mitigation requirement should be revoked. This regulatory trigger has now been met, according to CARB emission inventory models.

The Executive Order sunsetting the ADF regulation’s NOx mitigation requirement took effect January 1, 2026. The CARB action has been applauded by the Clean Fuels Alliance and other biofuel groups.

Indonesia scraps plan to introduce B50 biodiesel this year

Indonesia has scrapped plans for a mandatory B50 grade of palm oil-based diesel this year and will stick with B40 owing to technical and funding concerns, easing concerns over strains on global palm oil supplies.

Indonesia had planned to launch the B50 grade—a blend of 50% palm oil-based biodiesel and 50% conventional diesel—in the second half of this year. Its mandate for B40, which uses a blend of 40% palm oil-based biodiesel, will remain in place.

The government is reviewing the timeline to complete trials of B50 fuels, especially for trains, heavy equipment and machinery, energy ministry officials told reporters.

Indonesia subsidizes its biodiesel program to reduce the price gap between fuels made from crude oil and palm oil, using proceeds from palm oil export levies collected by the Indonesian Estate Crop Fund Agency (BPDP). The ever expanding mix, from B15 for only a few sectors in 2015 to B40 for nearly all diesel machines today, has put pressure on BPDP’s ability to subsidize the program.

To sustain the BPDP agency, the government will raise the levy rates. Indonesia will raise crude palm oil export levies to 12.5% starting from March 1. Levies for refined products will also be raised by 2.5 percentage points. Indonesia currently collects 10% levies on crude palm oil, with the rate for more refined products ranging between 4.75% and 9.5%.

Mercedes reaches $150 million settlement with US states over diesel scandal

Mercedes-Benz has reached a $149.6 million settlement with US states to resolve a long-running investigation into allegations of diesel emissions cheating by the automaker. Mercedes said the deal effectively ends its legal issues in the United States over dieselgate—the emissions scandal first uncovered at Volkswagen in 2015.

Under the settlement with 48 US states, Puerto Rico, and the District of Columbia, Mercedes will pay $120 million to the states. An additional $29,673,750 will be suspended and potentially waived pending completion of a comprehensive consumer relief program.

In addition, Mercedes will pay $2,000 and provide an extended warranty to eligible owners and lessees whose vehicles received required emissions repairs. The consumer relief program extends to an estimated 39,565 vehicles that had not been repaired or permanently removed from the road in the United States by August 1, 2023.

The states said Mercedes installed undisclosed unlawful software in diesel vehicles that hid the true levels of pollution and improperly lowered emissions during government testing.

100% of Delhi’s public transport buses to be converted to electric fleet

Delhi Chief Minister Rekha Gupta announced that within the next three years, 100% of Delhi’s public transport buses will be converted into an emission-free electric fleet, according to Indian media reports.

In a public address made on India Republic Day, Mrs. Gupta said, “The Delhi government has doubled its capital expenditure. ₹30 thousand crore [~3.2 billion USD] will now be spent on capital expenditure in Delhi. To make Delhi better, we have decided that within three years, 100 per cent of Delhi’s public transport buses will be converted into an emission-free electric fleet. All necessary arrangements have been made to ensure that Delhi receives 11,000 electric buses. The infrastructure required to maintain these electric buses, such as new charging stations and new bus depots, is being created rapidly.”

Ram unveils Power Wagon pickup with 6.7 L Cummins diesel engine

Stellantis’ Ram brand announced the first-ever availability of the 6.7 L Cummins High-Output (HO) turbo diesel in the Ram Power Wagon. Powered by the 6.7 L inline-six diesel engine, the new Power Wagon produces 430 hp (321 kW) and 1,075 lb-ft (1,458 Nm) of torque. Ram touts the vehicle as the most off-road-capable full-size pickup.

2027 Ram Power Wagon

The 2027 Ram Power Wagon has a tow rating of nearly 9,072 kg (20,000 lbs) and a payload capacity of almost 1,360 kg (3,000 lbs). The truck features a range of off-road technologies, offering front and rear electronic-locking differentials, Bilstein shocks, extensive underbody protection, five-link coil rear suspension, Hill Decent Control, Mopar® accessory rock rails, and disconnecting front stabilizer bar. A standard 117 L fuel tank enables an estimated 1,555 km (966 mile) range.

The Ram Power Wagon with Cummins turbo diesel will arrive in the second half of 2026. Stellantis said that vehicle pricing will be announced closer to launch date. According to press reports, prices will start at $88,470.

Ram will also launch the most powerful version of its TRX pickup, the 2027 Ram 1500 SRT TRX, according to media reports. The truck will be powered by a 6.2 L Hemi V8 gasoline engine producing 777 hp (579 kW) and 680 lb-ft (922 Nm) of torque.

The TRX truck—touted as the world’s “fastest and most powerful production gas pickup truck” in the half-ton segment—will accelerate from 0 to 60 mph (97 km/h) in 3.5 seconds. Like the Power Wagon, the 2027 TRX will be available in the second half of 2026 with prices starting at $99,995.

These two powerful pickup trucks are being released as the US government is relaxing fuel economy and GHG emission standards. In December 2025, the National Highway Traffic Safety Administration (NHTSA) proposed to relax the existing Corporate Average Fuel Economy (CAFE) standards for model year 2022-2031 vehicles. In July 2025, the Environmental Protection Agency (EPA) proposed to rescind the GHG Endangerment Finding—a landmark 2009 determination that greenhouse gases in the atmosphere are a threat to the public health and welfare. The latter action, if finalized, would repeal all GHG emission standards for light-, medium-, and heavy-duty vehicles and engines.

International announces EPA 2027 compliant S13 diesel engine

International Motors announced its 2027 S13® Integrated Powertrain meets the US EPA emission requirements for model year 2027 heavy-duty engines. Developed from a clean sheet design starting in 2017, the current platform of the S13 Integrated Powertrain was launched for the 2024 model year.

The 2027 S13 Integrated Powertrain carries over 90% of hardware from the current platform. The updated powertrain will provide similar fuel economy, driving experience, and powertrain weight as today’s S13 Integrated Powertrain, according to International.

2027 S13 diesel engine

The 2027 S13 engine features a less complex design, while meeting more stringent NOx emission standards: the 2027 NOx limit (FTP) is 0.035 g/hp-hr, compared to the current limit of 0.2 g/bhp-hr. The 2027 engine uses a dual-stage SCR aftertreatment without exhaust heaters, while exhaust gas recirculation (EGR) has been entirely eliminated. The current S13 engine uses a dual SCR system in combination with un-cooled EGR.

Several technologies remain unchanged from the current S13 platform, including:

Fixed-geometry turbocharger with “smart DEF dosing” (presumably Scania turbo dosing), dual overhead cam design, and 23:1 compression ratio.

T14® 14-speed transmission with planetary gearset, electronic clutch actuator, integrated PTO options, and advanced oil lubrication system.

Same size, packaging, and service intervals of the dual-stage aftertreatment system.

New technologies for 2027 include:

Variable Valve Timing (VVT), which enables Variable Valve Braking (VVB) for improved braking performance, closed crankcase breather, and oil centrifuge.

T14 Transmission: 24V Transmission Control Module with predictive shifting using GPS and topography data.

A standardized 24V electrical architecture across the entire powertrain platform (alternator, starter, and engine controllers). A 12V electrical system is retained for the cab and chassis, battery accessories, and body controls.

The S13 powertrain is approved for use with R100 renewable diesel. Trials for B100 biodiesel compatibility are underway.

The International S13 Integrated Powertrain is a collaboration with Scania, which together with International is part of the Volkswagen-owned Traton Group.

Volvo Penta debuts 17 L natural gas engine for power generation

At PowerGen 2026, held in San Antonio, Texas, Volvo Penta premiered its G17 natural gas engine, designed to provide reliable, scalable, and lower emission backup power for data centers, utilities and other mission-critical infrastructure.

Built on the same platform as the D17 diesel engine, the 17 L G17 six-cylinder, spark-ignited model is engineered to deliver approximately 450 kWe at 1,800 rpm.

The G17 is designed for reduced NOx and PM emissions. It utilizes advanced combustion controls, low-pressure exhaust gas recirculation (EGR), and a high-efficiency three-way catalyst.

Tata unveils 17 new trucks across diesel and electric portfolios

Tata Motors has expanded its commercial vehicle portfolio with 17 new diesel and electric trucks, covering payload categories from 7 tonnes to 55 tonnes, introducing new platforms, safety upgrades, and an electric truck range for varied applications.

The launch includes new products across the Prima, Signa, Ultra and the newly introduced Azura platforms, along with an expanded electric line-up under the Tata Trucks.ev brand.

The new range is aimed at applications across light, intermediate and heavy commercial vehicle segments, including logistics, e-commerce, FMCG distribution, construction, mining, agriculture, ports and regional freight operations.

A key addition to Tata Motors’ portfolio is the new Azura series, positioned in the intermediate and light commercial vehicle (ILMCV) segment. The Azura range will be offered in configurations ranging from 7 tonnes to 19 tonnes and is powered by a newly developed 3.6 L diesel engine.

The Azura trucks are targeted at medium-haul, intercity and regional transport applications, including last-mile logistics, white goods distribution, construction materials and agricultural goods movement.

Tata Motors has updated its entire diesel truck portfolio including the Prima, Signa, Ultra and Azura ranges to comply with ECE R29 03 crash safety standards. These regulations cover full-frontal impact, side impact and rollover protection for commercial vehicle cabins.

The updated trucks feature reinforced cabins and are equipped with multiple active safety systems. These include advanced driver assistance technologies such as lane departure warning, adaptive cruise control and collision mitigation systems. Safety-related driving behavior is monitored in real time through Tata Motors’ Fleet Edge connected vehicle platform.

The company has also introduced drivetrain updates across its heavy-duty diesel trucks, including improvements to its 6.7 L Cummins diesel engine range. Tata Motors claims fuel efficiency gains of up to 7% on certain models.

US NHTSA opens new investigation into GM’s 6.2 L V-8 engines

US safety regulators have escalated their scrutiny of General Motors’ 6.2 L V8 L87 engine, now targeting vehicles that allegedly failed after receiving the manufacturer’s prescribed remedy.

The National Highway Traffic Safety Administration (NHTSA) has opened Recall Query RQ26001, a direct investigation into the “adequacy of the remedy” for Recall 25V-274, which initially covered nearly 600,000 trucks and SUVs. This new action stems from 36 separate complaints in which engines catastrophically failed after a dealer inspection and service intended to prevent that exact outcome.

Recall 25V-274 addressed vehicles equipped with the L87 gasoline engine that experienced engine damage or failure. The recall’s remedy included an engine inspection. Based on the results of the inspection, the vehicle was to receive an oil change to a higher viscosity oil or an engine replacement. The complaints received by NHTSA allege failures of both remedies.

The engine has been used in several premium GM trucks and SUVs, including MY 2021–2024 Cadillac Escalade, Chevrolet Silverado, Chevrolet Suburban, and Chevrolet Tahoe.

Geotab: The updated guide to real-world EV battery health

Geotab, a Canada-based provider of telematics technologies, released an updated guide to real-world EV battery health. The analysis is based on over 22,700 electric vehicles, covering 21 different vehicle models, according to the company. The key insights are:

Average degradation rate: The average annual electric vehicle degradation rate is 2.3%.

Power: High-power DC fast charging (>100 kW) is the single largest stressor, leading to degradation rates up to twice that of the low power charging group (3.0% vs 1.5% per year).

Climate: Hot climates impose a penalty on battery life, with vehicles operating in hot conditions degrading 0.4% faster per year than those in mild climates.

Utilization: The increase in degradation from high daily use is a measurable but worthwhile trade-off for the gains in fleet productivity and ROI.

State of charge (SOC): For most EV use, there is no need to worry about avoiding fully charging or emptying the battery. Degradation only speeds up when vehicles spend over 80% of their total time at or near-full or nearly empty charge levels.

Donut Lab announces solid state battery ready for OEM use

Donut Lab, a Finnish developer of solid-state batteries, unveiled at CES 2026 a new high-performance solid state battery ready for OEM use. The battery is claimed to have 400 Wh/kg of energy density with a design life of up to 100,000 cycles. It can be charged to full in five minutes without limiting charging to 80%, and supports full discharge safely, repeatedly, and reliably.

At –30°C, the battery is claimed to retain over 99% of its capacity, and when heated to temperatures exceeding 100°C, it continues to retain over 99% capacity with no signs of ignition or degradation. The battery is made from abundant and geopolitically safe materials, does not rely on rare elements, and has a lower cost than lithium-ion batteries.

Donut Lab said its solid-state batteries are to be placed immediately on the road, powering Verge Motorcycles’ current lineup, including the Verge TS Pro and Ultra motorcycles.

However, battery experts remain skeptical about the claims. The chairman of Chinese battery manufacturer Svolt Energy said that Donut Lab’s claimed battery parameters are contradictory, and such a battery simply does not exist. “That battery doesn’t exist in the world,” Yang Hongxin, chairman and CEO of Svolt Energy, told local media, as reported by CnEVPost. “All the parameters are contradictory... Any technician with basic knowledge would recognize it as a scam.”

A.P. Moller–Maersk takes delivery of sixth 17,480-TEU methanol-capable ship

A.P. Moller–Maersk has taken delivery of Barcelona Mærsk, the sixth and final vessel in its 17,480-TEU dual-fuel methanol container ship series, according to media reports.

The vessel was name-given in Ulsan, South Korea, following construction carried out in collaboration with HD Hyundai Heavy Industries.

With this delivery, Maersk’s methanol-capable fleet has grown to 19 vessels, reaching the company’s deployment target by 2026. Maersk’s methanol fleet now comprises 12 vessels with a capacity of 16,000 TEU, six vessels with a capacity of 17,480 TEU and one 15,690-TEU container ship that has been retrofitted to operate on methanol.

The company has also ordered six 9,000-TEU methanol-capable vessels, which are scheduled for delivery by Yangzijiang Shipbuilding by 2027.

Maersk has positioned methanol as a key alternative fuel in its decarbonization strategy for container shipping, with the dual-fuel vessels designed to operate on both conventional marine fuels and methanol.

Wärtsilä 25 Ammonia engine to power Skarv Shipping’s first newbuild cargo vessel

Wärtsilä announced it will provide its Wärtsilä 25 Ammonia engine to power a new cargo vessel for Norway-based Skarv Shipping Solutions. The vessel will be constructed at China’s Huanghai shipyard and will become the first newbuild fitted with Wärtsilä’s full ammonia propulsion package.

The scope covers the Wärtsilä 25 Ammonia engine, the AmmoniaPac Fuel Gas Supply System, the Wärtsilä Ammonia Release Mitigation System and a selective catalytic reduction (SCR) system designed for ammonia.

Total GHG emissions are reduced by at least 90% when running the engine on “sustainable ammonia”, compared to equivalent diesel engines, according to Wärtsilä. This allows operators to meet current EU emissions targets for 2050, and to also exceed the IMO target for 2040.

The order was booked in the fourth quarter of 2025. Equipment deliveries for the newbuild are scheduled to begin in the fourth quarter of 2026.

Iveco Bus delivered its hydrogen city bus, the GX 337 H2 LINIUM, to the Lorient Agglomeration (France), marking the first European delivery of the vehicle. The GX 337 H2 LINIUM features a 100 kW fuel cell powered by four hydrogen tanks, paired with a 69 kWh FPT Industrial battery pack. The bus can carry up to 110 passengers and has an operational range of up to 450 km. Further deliveries are planned over 2026, with a total of up to 19 H2 fuel cell buses set to join the fleet.

Daimler Truck will produce 100 units of its new hydrogen-powered semi-trailer tractor, the Mercedes-Benz NextGenH2 Truck, at the Mercedes-Benz plant in Wörth. The truck uses two fuel cell units, delivering a total output of 300 kW. In tests, the hydrogen consumption averaged between 5.6 and 8 kg per 100 km on vehicles with a gross combined weight of between 16 and 34 tonnes. Liquid hydrogen enables ranges well over 1,000 km on a single tank filling of 85 kg. A 101 kWh Li-ion phosphate (LFP) battery pack stores energy from the fuel cells and also from brake regeneration. The fuel cell trucks will be deployed with various customers from the end of 2026.

Otto Zimmermann details Euro 7-compliant brake parts

The Euro 7 emission regulation—effective 2026.11.29 for new type approvals—includes, for the first time ever, certain requirements for non-exhaust particle emissions from light-duty vehicles, including brake wear particles. To meet these emission requirements, German parts supplier Otto Zimmermann has updated its product range to reduce particulates released by brake pads and discs.

To meet the new brake particle emission limits, Zimmermann relies on advanced coating and friction partner technologies:

Carbide-coated brake discs: These highly wear-resistant coatings significantly reduce abrasion.

Optimized friction mixtures: Special formulations reduce the proportion of fine particles during braking.

Closed braking systems such as drum brakes are also considered a possible addition. Otto Zimmermann has been offering brake drums for the aftermarket in this sector for over six decades. The relatively closed system allows brake drums to better retain fine dust.

For more than 100 years, crude oil has been essential for almost every sector of the economy and a powerful force in shaping the history of the modern world, as described by Matthieu Auzanneau in his excellent book Oil, Power, and War. However, the oil interest has typically acted in the background, hidden from public view. Now, unlike past interventions, the United States has made it clear that oil has been among the key motives behind the January 3rd attack on Venezuela.

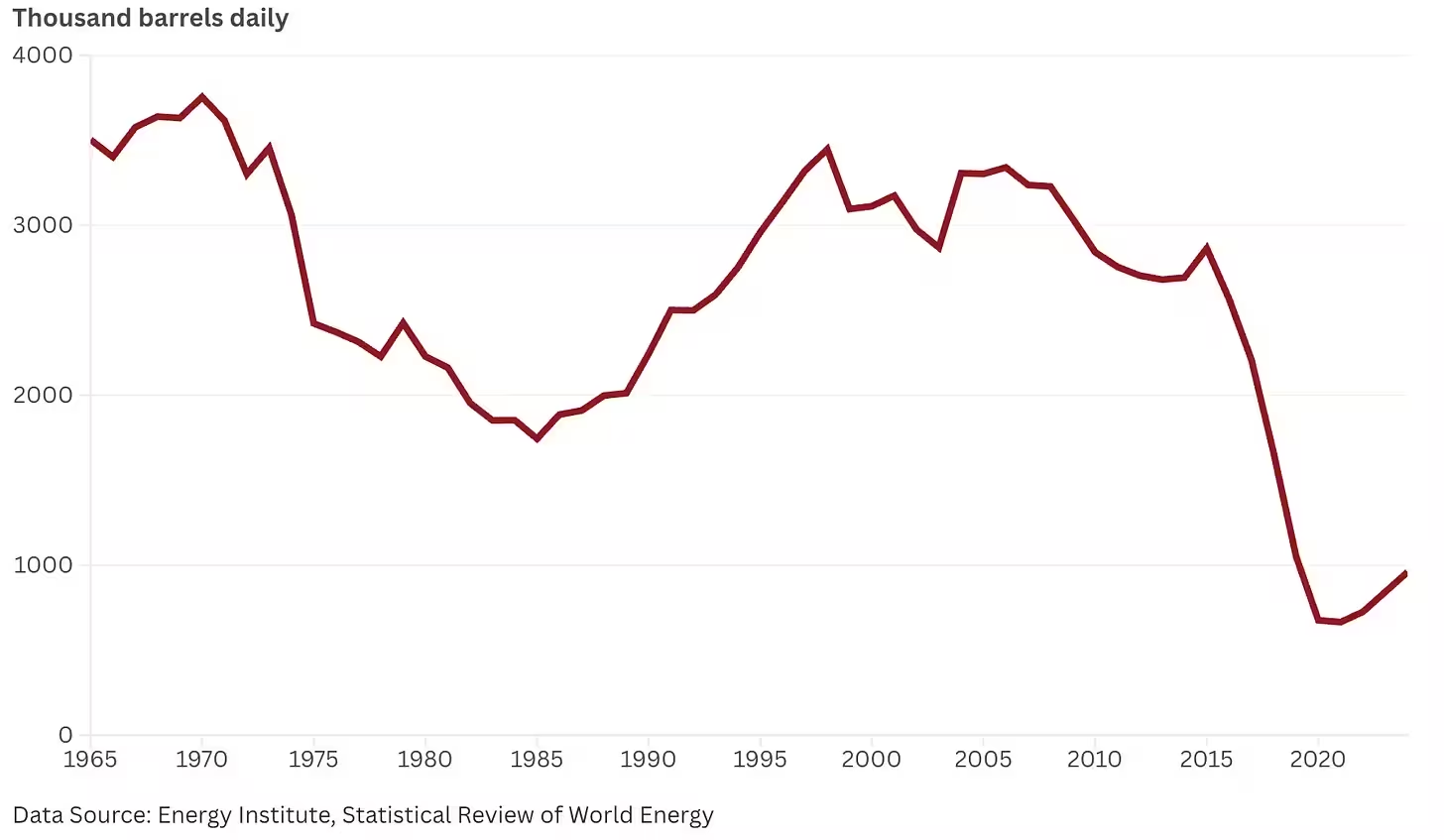

Venezuelan oil output reached its peak in 1970. After several decades of ups and downs, the oil production entered a free-fall phase in 2015. While a recovery began around 2020, Venezuela—with an output of approximately 1 million barrels per day (b/d)—is struggling to secure a place among the world’s top ten oil producers.

The decline of Venezuela’s oil output is often attributed to decades of underinvestment, nationalization, sanctions, and infrastructure decay. Most likely, these factors have all played a role. In 2006/2007, Venezuela finalized the Majority State Ownership clause in their Constitution, which led to a seizure of the assets of ExxonMobil, ConocoPhillips, and other Western oil companies and their exodus from the country. The nationalized oil company, Petróleos de Venezuela S.A. (PDVSA), suffered a significant loss of technical expertise. However, another important factor contributing to the slump in oil production has been depletion of light oil resources.

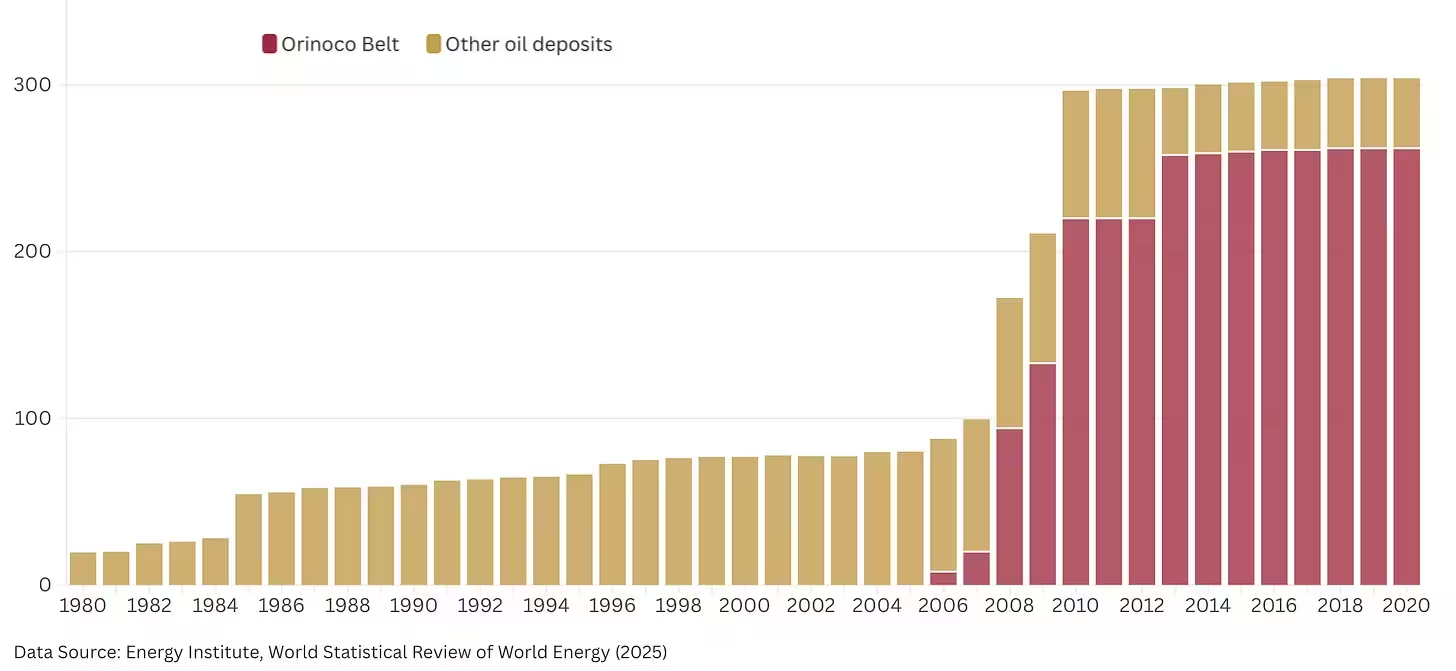

Venezuela has the highest crude oil reserves in the world, claimed to be 304 billion barrels—ahead of Saudi Arabia (298 billion), Canada (168 billion), and Iran (145 billion). These reserves—which are not audited and the recovery rates of which are debatable—have been increased on several occasions. In 1986, Venezuela suddenly increased its reserves together with other OPEC countries, which led to a widespread upward re-evaluation of the respective countries’ OPEC oil export quotes.

From 1986 to 2007, reserves grew to 100 billion barrels. But the largest jump occurred over the period of 2008-2011. By January 2011, reserves reached 297 billion barrels—when the heavy oil from the Orinoco Belt formation was classified as proved oil reserves, while light-oil reserves have been declining.

The Venezuelan Orinoco Belt resources are classified as extra heavy crude—very high density oil (6-10°API) that cannot easily flow under normal conditions, similar to the Canadian Athabasca crude extracted from oil sands. The extraction of heavy crude oil and bitumen requires specialized technologies such as open pit mining or in-situ thermal extraction by steam injection. Then the heavy oil needs to be upgraded to a lighter product that can be transported via pipelines. Venezuela used to produce some lighter crudes, which were largely used as diluents for the heavy oil, but these fields are now largely depleted and Venezuela now needs to import light material to act as diluent. To make the project more challenging, the Orinoco oil sands are located in a jungle, a rather difficult place to work.

The United States actually needs heavy oil, because US shale oil—which is about two-thirds of total US output—is very light, suitable for the production of gasoline but not particularly suitable for diesel fuel. However, the extraction of heavy oil requires a long term investment to develop the necessary infrastructure, as well as sufficiently high oil prices to be profitable.

Chevron is currently the only oil major with some operational presence in Venezuela. The US administration has been encouraging oil companies to invest at least $100 billion to rebuild Venezuela oil industry but major US oil executives remain cautious, with the head of Exxon Mobil calling the nation currently “uninvestable.”

The development of the Orinoco Belt resources would require a long term investment—it took Canada several decades to develop Alberta oil sands—but the political stability and investment security are not assured. Since oil extraction by Western companies was already intervened in 2007, no one can ensure that the same situation cannot be repeated, considering that the contracts would be signed by the Venezuelan authorities under coercion. And the US administration has no plans to directly provide security guarantees to oil producers in Venezuela, according to the Energy Secretary Chris Wright.

It has also been noted that the Venezuelan oil infrastructure produces vast methane leaks, which could scare off some groups of international investors.

Still another limitation on the control of Venezuelan oil exports is presented by China. Despite holding a relatively modest share of Venezuela’s total external debt—roughly $10-12 billion—much of China’s exposure is collateralized by oil shipments. That structure gives Beijing leverage to delay or complicate a comprehensive debt restructuring, particularly if it prefers continued oil-backed repayments to accepting a haircut.

Crude Oil. Prices increased over the month, driven by cold weather that reduced US production and Gulf Coast crude exports, and by the specter of a war with Iran. Additionally, oil supply was tightened by a fire at Kazakhstan’s Tengiz field. On January 29th, WTI futures traded at $65.42 per barrel and Brent at $69.59.

The US Energy Information Administration (EIA) posted its global monthly oil output data for September 2025, showing another record high of 86,033 million b/d. A big contributor to this increase was Saudi Arabia. The global oil production first surpassed its prior peak of November 2018 (84.593 mb/d) in July 2025 (84.726 mb/d) and increased further in August (85,297 mb/d) and in September (86,033 mb/d).

In its latest Oil Market Report, the International Energy Agency forecast global oil demand would expand by 930,000 b/d in 2026, up from 850,000 b/d in 2025, reflecting a normalization of economic conditions after last year’s tariff turmoil and lower oil prices than a year ago.

Forecasts for a massive oversupply of crude oil in 2026 are beginning to soften. According to Saudi Aramco’s CEO, Amin Nasser, oil glut forecasts are seriously exaggerated as demand keeps rising and global stocks are below the five-year average. Moreover, spare capacity has dwindled over the past year, also limiting potential efforts to boost output in case of major supply disruptions.

In the January 2026 Short-Term Energy Outlook, the EIA forecasts that US crude oil production next year will remain near the record 13.6 mb/d produced in 2025 before decreasing 2% to 13.3 mb/d in 2027. If realized, a fall in annual US crude oil production will mark the first since 2021.

As cold weather strains electric grids across the United States, operators are considering ordering data centers to run diesel-powered backup generators, a move that threatens to push prices for distillate fuel up further. On January 26, the US DOE authorized PJM Interconnection, the country’s largest power grid operator, and two units of Duke Energy to direct data centers and other large facilities to run backup generators as a last resort to prevent rolling blackouts. The move effectively allows power destined for industrial-scale customers to be diverted to households and the rest of the grid as heating demand tests the upper limits of electricity supplies.

Russia’s diesel exports experienced a significant increase in December 2025, rising by approximately 36% to 40% month-on-month to reach a four-to-six-month high of around 900,000 to 988,000 b/d. This surge marked a recovery from a five-year low in September 2025 and was apparently driven by higher refining throughput as refineries repaired damage from earlier drone attacks.

Middle East diesel exports to Europe in 2025 exceeded 500,000 b/d for the first time, with Saudi Arabia leading the way, according to the latest ship-tracking data. Diesel shipments averaged 519,000 b/d last year compared with 497,000 b/d in 2024. Saudi Arabia’s diesel exports averaged 311,000 b/d, nearly three times the volume of the second-largest exporter, Kuwait, which shipped 110,000 b/d. France was the top destination. In December, diesel exports from the Middle East rose to 459,000 b/d from 352,000 b/d in November, the data showed.

Natural Gas. Winter Storm Fern has been associated with some of the fastest rise in US gas prices, with Henry Hub futures exceeding $7 per million BTU on January 26th and Henry hub spot prices exceeding $30 per million BTU. On January 29th, Henry Hub futures traded at around $3.78 per million BTU. In Europe, Dutch TTF natural gas futures for the front month closed at €40.11/MWh (~$14 per million BTU), compared to €28.16/MWh on December 31st.

Europe’s underground gas storage is emptying faster than normal this winter, and the rapid drawdown is pushing up prices. With the winter heating season just half-way through, storage sites are less than 50% full on average down from almost 83% when winter started on October 1. The fill rate is the second lowest for the time of year in the last ten years and 13 percentage points lower than average.

The European Union is on track to get nearly half its gas from the United States by the end of the decade, creating a major strategic vulnerability for the bloc as relations with Washington hit an all-time low, writes Politico. Europe is already importing a quarter of its gas from the USA, a figure that is set to soar as the bloc implements a total ban on Russian gas imports.

The rules to phase out Russian gas imports will apply to different kinds of gas in phases. Spot market purchases of gas will be banned almost immediately—from six weeks after entry into force of the regulation—while existing short- and long-term contracts will be banned over a period from April 2026 to September 2027, depending on the type of gas (pipeline vs LNG) and the type of the contract.

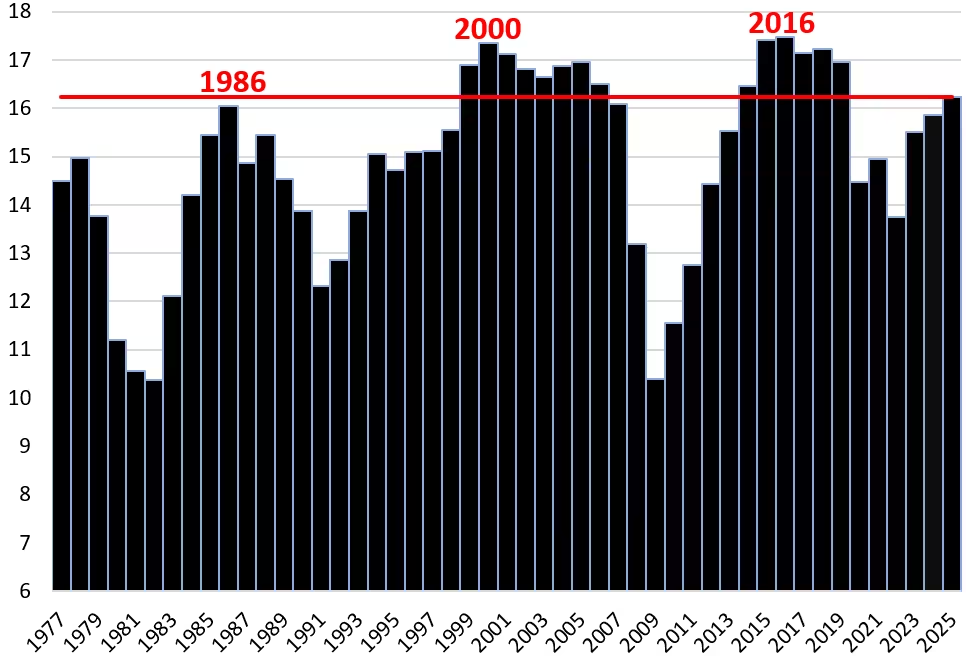

Automotive Industry. In the United States, total new-vehicle sales rose by 2.4% in 2025 to 16.2 million vehicles, the highest since 2019, and just a hair above where sales had been four decades ago, in 1986. The two best years were 2000 and 2016, with 17.4 million and 17.5 million vehicles sold. In 2025, sales were 6.4% below the year 2000. Over those 25 years, the US population has increased by 21%.

Stellantis FCA continued its declining trend, with sales dropping further in 2025, down by 44% from the high in 2015; Nissan may have paused its decline, with sales roughly flat year-over-year, and down 42% from the 2017 high. GM’s and Ford’s sales have both increased, but are still well below their 2015 levels. Honda also eked out a gain for the year, but sales were still down 13% from the peak in 2017. Toyota’s sales jumped and surpassed its 2015 record by a hair. Hyundai-Kia sales continued to surge from record to record [charts].

US vehicle prices exploded during 2020-2022 and then stabilized. The average retail transaction price peaked at the end of 2022 at $47,329 and has remained roughly at that level since then. At the end of 2025, the average transaction price was $47,104, up by 1.5% from a year ago, and down by 0.5% from three years ago.

While BEV market share reached an all-time high in September, sales cooled significantly once tax credits were no longer available. By December, BEV market share fell to 5.9%, a decline of 5.9 percentage points compared to the record set in September. For all of 2025, BEV sales total 1.26 million units, an increase of 1.2% compared to 2024. Despite the increase in BEV sales, BEV market share declined year-over-year by 0.1 percentage points to 7.7% in 2025.

The total number Tesla vehicle deliveries to customers around the globe in Q4 2025 declined by 15.6% from a year ago, to 418,227 vehicles, the lowest Q4 since 2022. Deliveries of the Model 3 and Model Y plunged by 13.8% from a year ago, to 406,585 vehicles, also the lowest Q4 since 2022 (blue).

Deliveries of what Tesla calls “other” models—Cybertruck, Model S, and Model X combined, the green line at the bottom of the chart—collapsed by 50.8% year-over-year to just 11,642 vehicles in Q4. The Cybertruck can now be described as a failed model. On the other hand, the Model Y remains an immensely successful model in the USA: In 2025 through Q3, it was the #1 bestseller by registrations, with a share of 3.0% of all vehicles sold, ahead of the Toyota RAV4 (2.9%), and the Ford F-150 pickup (2.8%).

In the European Union, in 2025, new car registrations reached 10.82 million vehicles, an increase of 1.8% compared to 2024. However, overall volumes remain well below pre-pandemic levels. Battery-electric cars accounted for 17.4% of the EU market share in 2025, an increase from 13.6% one year earlier. Hybrid-electric car registrations captured 34.5% of the market, remaining the preferred choice among EU consumers. Meanwhile, the combined market share of petrol and diesel cars fell to 35.5%, down from 45.2% in 2024.

The EU’s commercial vehicle market had a challenging year in 2025, with registrations falling across several major markets, a clear sign of the tough economic environment. The bus segment was the only exception.

New EU van registrations fell by 8.8%, with the three largest markets contributing to the downturn. France recorded the steepest drop with an 5.6% decline, followed by Germany (‑5.4%) and Italy (-5%). In contrast, Spain saw a surge in registrations, rising by 11.7%.

New EU truck registrations also fell by 6.2%, totaling 307,460 units. This downturn was driven in volume by a 5.4% decline in heavy-truck registrations, alongside a 9.9% decrease in medium-truck demand. All major markets contracted, with Germany (-12.2%) experiencing double-digit decline, followed by France (-9%) and Spain (-3.6%).

Meanwhile, new EU bus registrations grew 7.5% in 2025, reaching a total of 38,238 units. Among major markets, growth was led by Germany (+28%) and Poland (+16.6%), while Italy (-15.9%) and Spain (-4%) continued to see declines.

In China, in 2025, automobile production and sales exceeded 34 million vehicles, a record high. The production and sales of new energy vehicles (NEV) have exceeded 16 million, and the domestic NEV sales account for more than 50%.

Chinese EV exports increased by 87% in November 2025. The top export destinations included Maxico (19,344 units), Indonesia (17,503), and Thailand (13,517). In 2025, over 600,000 Chinese EVs have been exported to Europe.

In the UK, Tesla’s car registrations dropped by more than 29% year-on-year in December, underscoring the intense competition from Chinese rivals.

BP sells majority stake in Castrol for $10 billion

BP has reached an agreement to sell a 65% shareholding in Castrol lubricants business to Stonepeak at a $10 billion enterprise value, generating roughly $6 billion in net proceeds.

Upon completion of the transaction, a new joint venture will be incorporated comprising a 65% Stonepeak and 35% BP ownership. Following a two-year lock-up period, BP has optionality to sell its 35% stake in Castrol.

BP plans to apply the entire amount of the net proceeds toward reducing net debt, which stood at $26.1 billion at the end of Q3 2025. The transaction also simplifies BP’s downstream operations and advances its reset strategy of focusing capital on integrated businesses with higher returns.

The divestment comes as BP moves to tighten its balance sheet, optimize its portfolio, and improve cash generation. The company has now completed or announced more than half of its $20 billion divestment program, with cumulative proceeds at approximately $11 billion.

Castrol—founded 126 years ago—remains one of the world’s most recognized lubricant brands, with material market positions across automotive, industrial, and marine sectors. The new joint venture structure allows BP to retain exposure to Castrol’s growth trajectory. Castrol posted nine consecutive quarters of year-over-year earnings growth.

Regulatory approvals are expected to be completed by the end of 2026.

BP flags up to $5 billion in low-carbon energy impairments

BP expects to book $4 billion to $5 billion in fourth-quarter impairments, mainly tied to its low-carbon energy businesses, as it redirects spending to oil and gas to boost returns. A BP spokesperson declined to say which projects were affected.

BP’s low-carbon portfolio also includes US biogas producer Archaea which BP bought in 2022 for $4.1 billion. Citi analysts said they suspected impairments might be linked to this unit.

After taking a $24 billion hit from exiting Russia in 2022, BP—with a current market capitalization of around $91 billion—recorded impairments of $5.7 billion in 2023, $5.1 billion in 2024 and has flagged around $6.9 billion for last year, according to its releases and Reuters calculations.

The company reduced its annual spending on energy transition businesses about a year ago from $7 billion to a maximum of $2 billion as it embarked on a major strategy shift back to oil and gas.

Honda to boost output of cheaper gasoline vehicles

Honda Motor plans to increase production of cheaper gasoline-fueled vehicles for the US market, a reflection of the ongoing relaxation of US emission and fuel economy standards and a new-car affordability crisis.

The Japanese carmaker’s sales of electrified vehicles will take a back seat to gasoline-fueled cars and SUVs in response to growing demand for low-cost models, Lance Woelfer, the head of Honda’s US sales operations, said in a media briefing.

“We’re actually going to increase production of more affordable trims this year to make sure we can meet the needs of our customers. This means adjusting our production mix to include more lower-priced, gas-powered models,” he told reporters. “Every manufacturer is talking about affordability being one of the main challenges in the marketplace.”

The move comes as many American car buyers are struggling to afford new-car prices that average nearly $50,000, and as the auto industry embraces less stringent US federal rules on internal combustion engines and relaxed Corporate Average Fuel Economy (CAFE) requirements.

Hybrids, which typically cost more than gas-only models, made up a large share last year of Honda’s most popular models, including 54% of its CR-V crossovers, half of Accord midsized sedans and 36% of Civic compacts. But the additional upfront costs for more fuel efficient powertrains could take longer to pay off due to falling prices at the pump, as US gasoline prices have fallen to the lowest levels in at least a year.

A 2026 base model CR-V starts at around $32,370 in the USA, about $5,000 less than the lowest-priced hybrid version of the vehicle. A gasoline-fueled CR-V averages a combined city-highway 30 mpg, while the hybrid’s fuel economy is 10 mpg higher.

General Motors said it would take a $6 billion charge to unwind some electric vehicle investments, the latest car company to pull back from EVs in response to the current US policies and fading demand.

The charge stems from reducing its planned EV production and the fallout on the supply chain, and comes weeks after rival Ford Motor announced a similar but much bigger charge.

Most of GM’s writedown—a $4.2 billion cash charge—is related to contract cancellations and settlements with suppliers, who had planned for much higher production volumes.

The writedown would not affect GM’s US lineup of roughly a dozen EV models. “We plan to continue to make these models available to consumers,” GM said in its filing.

The company will record the charge as a special item in its fourth-quarter earnings report. It expects to incur additional charges in 2026 as a result of negotiations with its supply base, but expects them to be less than its 2025 EV charges.

China and the EU took a significant step toward easing their electric vehicle trade dispute after the European Commission released a guidance document that could allow Chinese exporters to replace punitive tariffs with negotiated pricing commitments.

The European Commission said companies may submit price undertakings that must be “adequate to eliminate the injurious effects of the subsidies and provide equivalent effect to duties”. Exporters are encouraged to include shipment limits and future EU investments, with assessments conducted under WTO rules. If accepted, the EU would revise its existing regulations.

The conflict dates back to the EU’s 2023 anti-subsidy investigation, which resulted in 2024 with the imposition of definitive countervailing duties ranging from 7.8% to 35.3% for five years. China responded with investigations into European cognac, dairy, and pork. The new framework could replace the tariffs with minimum import prices.

Canada and China reached a Preliminary Agreement-In-Principle that will reduce tariffs on electric vehicles and canola, as both nations promised to tear down trade barriers while forging new strategic ties during Canada’s Prime Minister Mark Carney’s visit to Beijing.

Canada will initially allow in up to 49,000 Chinese EVs at a tariff of 6.1% on most-favored-nation terms. This compares with the 100% tariff on Chinese EVs imposed in 2024, following similar US penalties. In 2023, China exported 41,678 EVs to Canada.

“This is a return to levels prior to recent trade frictions, but under an agreement that promises much more for Canadians,” Carney told reporters. He later said the quota would gradually increase, reaching about 70,000 vehicles in five years.

Relaxing EV tariffs diverged from US policy, and some members of US President Trump’s cabinet criticized the decision ahead of an expected review of the US-Canada-Mexico trade deal.

Premier Doug Ford of Ontario, Canada’s main auto manufacturing province, denounced the deal.

“The federal government is inviting a flood of cheap made-in-China electric vehicles without any real guarantee of equal or immediate investments in Canada’s economy, auto sector or supply chain,” he said in a post on X.

Under the new deal, Canada expects that China will lower tariffs on Canadian canola seed to a combined rate of approximately 15%. The current combined tariff level on canola is 84%. It was introduced by China in retaliation against Canadian tariffs on Chinese EVs, steel, and aluminum.

Japan’s TEPCO restarts first nuclear reactor since Fukushima

Tokyo Electric Power Company (TEPCO) restarted a reactor at the Kashiwazaki-Kariwa nuclear power plant. TEPCO put online the 1.36 GW reactor No. 6, one of seven at Kashiwazaki-Kariwa, once the world’s biggest nuclear power plant with a nameplate capacity of 8.2 GW.

The move marks the first reactor restart by TEPCO—Japan’s largest utility—after the 2011 earthquake and tsunami that led to the major nuclear accident at the company’s Fukushima Daiichi power plant.

Kashiwazaki-Kariwa reactor No. 6 is expected to restart commercial operation by the end of February. Reactor No. 7 is expected to be brought online around 2030, while some other reactors at the Kashiwazaki-Kariwa power plant can be decommissioned.

The restart of Kashiwazaki-Kariwa brings the total number of reactors currently in operation in Japan to 15, according to the World Nuclear Industry Status Report. A further 18 reactors are shut down but remain operable after the shutdown of Japan’s entire fleet of 54 reactors in the wake of the Fukushima Daiichi accident.

Japan now looks to have 20% of its electricity generation coming from nuclear power by 2040, up from 8.4% today.

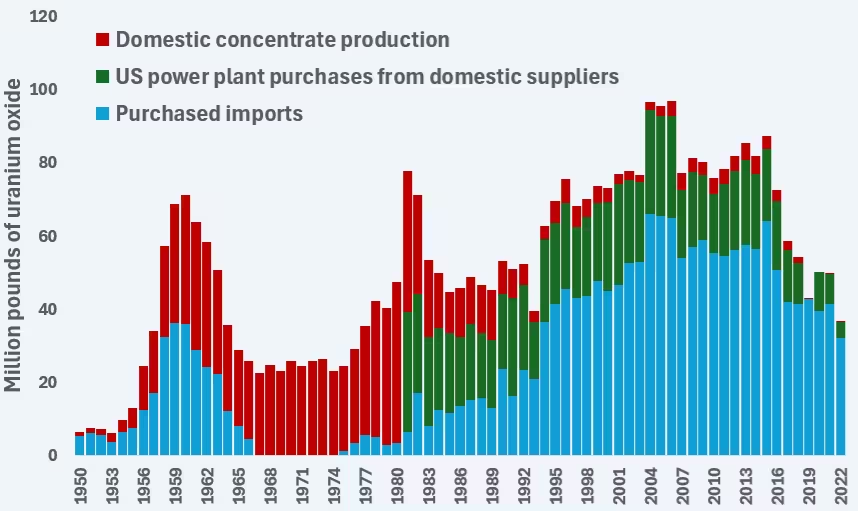

US awards $2.7 billion to boost uranium enrichment

The US Department of Energy (DOE) announced it was awarding orders totaling $2.7 billion to three companies to boost domestic uranium enrichment over the next 10 years.

The investment is intended to expand US capacity for low-enriched uranium (LEU) and jumpstart new supply chains for high-assay low-enriched uranium (HALEU).

Russia is currently the only country that makes HALEU—uranium enriched to between 5% and 20%—in commercial volumes. US nuclear powerplants rely on imported fuel, including uranium imports from Russia. Funds to make the fuel domestically in the United States were included in a law to discontinue uranium shipments from Russia by 2028.

The following companies were awarded orders totaling $2.7 billion to provide enrichment services for LEU and HALEU:

American Centrifuge Operating ($900 million) to create domestic HALEU enrichment capacity

General Matter ($900 million) to create domestic HALEU enrichment capacity

Orano Federal Services ($900 million) to expand US domestic LEU enrichment capacity

The DOE separately awarded an additional $28 million to Global Laser Enrichment, part-owned by Canadian uranium company Cameco, to further its work to build next-generation uranium enrichment technology for the nuclear fuel cycle.

HALEU’s critics say the technology presents a weapons risk and recommend limiting enrichment to between 10% and 12%. Uranium fuel used in most of today’s reactors is enriched to about 5%.

China has banned the export of several rare earth minerals to Japan over controversial remarks made by Japan’s Prime Minister regarding Taiwan. China has banned exports of dual-use items, including certain rare earth elements, to Japan, effective immediately. Dual-use items include technologies, goods or software with both civilian and military applications.

Beijing’s latest move is a reaction to controversial remarks made by Japan’s Prime Minister about Taiwan. In November 2025, Japanese Prime Minister Sanae Takaichi stated that a potential Chinese military attack on Taiwan could legally be considered a survival-threatening situation for Japan. China has demanded that Japan’s PM retract the remarks. However, Takaichi remains adamant, prompting a series of countermeasures by Beijing.

The WSJ reported that China began restricting exports to Japanese companies of “heavy” rare earths, as well as rate earth magnets. The review of applications for export licenses across Japanese industry has been reportedly halted. Japan is importing 60% of its rare earths from China and is almost totally dependent on Chinese imports for some heavy rare earths used for magnets in electric and hybrid vehicle motors.

China exerts near-total control over the global rare earths sector, dominating mining (around 70%) and holding a virtual monopoly (over 90%) in crucial downstream processing, refining, and magnet manufacturing, creating significant supply chain vulnerability for high-tech industries like defense, EVs, and AI. This dominance stems from decades of state-backed investment and vertically integrated supply chains, giving them power over the entire process from raw ore to finished component.

“Humans have depleted global terrestrial carbon stocks by a quarter”. Land-use activities such as agricultural expansion and forest management are massively altering vegetation and soil carbon stocks, releasing vast amounts of carbon into the atmosphere, which substantially contribute to global warming. Researchers from the University of Munich estimate that, globally, carbon in vegetation and soil has been reduced through land-use activities by 24% (344 PgC)—an amount comparable to all fossil fuel emissions over the past 50 years. The study also finds that current global vegetation models considerably underestimate this loss.

“Ambient air quality and health impacts of PM2.5 from US residential wood combustion”. A study by the Northwestern University, Illinois, suggests that residential wood combustion (RWC) makes a substantial contributions to PM2.5 pollution in metropolitan areas. While RWC is a primary heating fuel in just 2% of US homes, it contributes ~28% of total wintertime PM2.5 emissions. RWC is estimated to produce around 485,000 tons of primary PM2.5 annually, which amounts to more than double the total estimated primary PM2.5 emissions of the transportation sector.

“Identifying high-emitting Euro 7 vehicles with the NOx-to-fuel mass ratio”. Researchers from the University of València examines the introduction of the NOx-to-fuel mass ratio in the Euro 7 regulation, a parameter designed to evaluate the effectiveness of the vehicle emission control by assessing the mass of NOx emitted relative to fuel consumption. The study reviews in detail the methodology utilizing data from an on-road Euro 6d-Temp diesel vehicle.

“Emissions characteristics of amines and ammonia from typical diesel vehicles regulated by advanced post-treatment systems”. Chinese researchers present a quantification of species-resolved amines and NH3 emission factors across units of China VI typical aftertreatment system in diesel vehicles.

“Catalyst Deactivation Modes of Palladium Oxide on Gamma Alumina Catalysts for Lean Methane Oxidation”. A research team led by the Oak Ridge National Laboratory investigated the deactivation of Pd methane oxidation catalysts by water. Four catalyst deactivation modes were identified. Two of the deactivation modes are directly related to water, either from the feed gas or as a part of the reaction products, with one being attributed to the formation of surface hydroxyl groups and the other to the competitive adsorption of water on the catalysts. The impact of these two deactivation modes is severe but reversible. In contrast, two other deactivation modes are gradual and persistent but irreversible. Both modes are induced by methane oxidation reaction, with the impact of a wet feed being substantially more severe than that of a dry feed. The major cause of the irreversible catalyst deactivation is attributed to surface reconstruction of palladium(II) oxide nanoparticles, which behaves as a passivation layer lowering the number of coordinately unsaturated palladium sites for methane activation.

“Direct Air Capture: Recyclability and Exceptional CO2 Uptake Using a Superbase”. A new method to capture carbon dioxide from ambient air has been developed by researchers at the University of Helsinki.

GCMD: “Life cycle assessment finds significant emissions savings potential across the onboard carbon capture value chain”. The Singapore-based Global Centre for Maritime Decarbonisation (GCMD) has published an LCA of the GHG emissions from Project CAPTURED that involved ship-to-ship offloading of onboard captured and liquefied CO2 with downstream utilization, completed in June 2025.

NACFE: “The Idle-Reduction Playbook: Operational Strategies for Modern Trucking Fleets”. The North American Council for Freight Efficiency (NACFE) has released a new report on idle reduction. This is the second update to the initial idle reduction Confidence Report published by NACFE in 2014. The report covers a variety of idle-reduction technologies including diesel and electric APUs, fuel-operated heaters and coolant heaters, intelligent engine management systems, thermal management systems, vehicle controls, and driver behavior.

ACEA: “Vehicles on European roads 2026”. The report provides key data, including average vehicle age, vehicle power types, vehicle ownership patterns, and more essential information for understanding the automotive sector landscape.

ACEA: “Local Content Requirements for heavy-duty vehicles: ACEA’s guiding principles and policy recommendations”. The introduction of EU’s Local Content Requirements (LCRs) raises important considerations for European vehicle manufacturers. As heavy-duty vehicles (HDVs) have distinct characteristics, ACEA has developed specific guiding principles and policy recommendations for the HDV sector.

Wood Mackenzie: “Is Greenland Venezuela 2.0?” Greenland’s mineral resources include deposits of iron ore, copper, graphite, zinc, gold and uranium. In addition, the Gardar alkaline province in southern Greenland as holding prolific rare earth elements (REE), along with lithium, tantalum, niobium and zirconium. It is these resources that have caught the attention of the Trump administration, with officials speaking publicly about Greenland’s REEs offering a solution to China’s dominance. Here, ambition runs up against reality. Around 80% of the island is covered by the Greenland Ice Sheet, averaging a mile thick, meaning only limited work has been undertaken to quantify the true scale of Greenland’s deposits. Global mining companies might covet Greenland’s critical minerals, yet today there are only two operating mines across the entire country—the Nalunaq gold mine and an anorthosite mine on Greenland’s west coast.

Reggie Zhan: “Upcoming Automotive Emissions, Efficiency, and Safety Standards - China”. A list of anticipated upcoming Chinese regulations on emissions, fuels, NEVs, and emission compliance.

Technology Guide: Updated paper on diesel fuel ignition quality testing—added discussion of the most recent test methods for the determination of cetane number and related ignition quality parameters.

Technology Guide: The updated paper on Non-Exhaust Particle Emissions now covers the findings of the recent Ricardo report on brake and tire wear emissions.